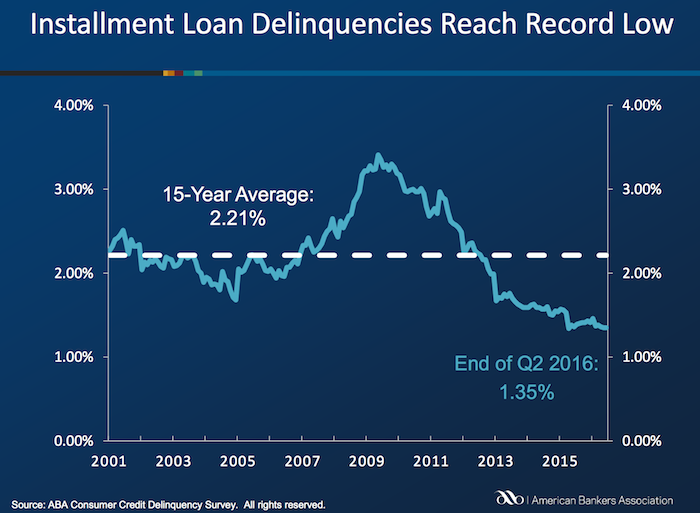

Delinquencies in closed-end loans fell slightly in the second quarter, driven by a drop in home equity loan delinquencies, according to results from the American Bankers Association’s Consumer Credit Delinquency Bulletin.

The composite ratio, which tracks delinquencies in eight closed-end installment loan categories, fell 3 basis points to 1.35% of all accounts – a record low. This also marked the third year that delinquency rates were below the 15-year average of 2.21%. The ABA report defines a delinquency as a late payment that is 30 days or more overdue. This is good news but the personal financial health of consumers in the USA is still in need of significantly improvements to their balance sheets. Debt levels are still too high. Savings levels are still far to low.

Home equity loan delinquencies fell 4 basis points to 2.70% of all accounts, which helped drive the composite ratio down. Other home related delinquencies increased slightly, with home equity line delinquencies rising 6 basis points to 1.21% of all accounts and property improvement loan delinquencies rising 2 basis points to 0.91% of all accounts. Home equity loan delinquencies dipped further below their 15-year average of 2.85%, while home equity line delinquencies remained just above their 15-year average of 1.15 percent.

Bank card delinquencies edged up 1 basis point to 2.48% of all accounts in the second quarter. They remain significantly below their 15-year average of 3.70 percent.

The second quarter 2016 composite ratio is made up of the following eight closed-end loans. All figures are seasonally adjusted based upon the number of accounts.

Closed-end loans

Home equity loan delinquencies fell from 2.74% to 2.70%.

Mobile home delinquencies fell from 3.41% to 3.17%.

Personal loan delinquencies fell from 1.44% to 1.43%.

Direct auto loan delinquencies rose from 0.81% to 0.82%.

Indirect auto loan delinquencies rose from 1.45% to 1.56%.

Marine loan delinquencies rose from 1.03% to 1.23%.

Property improvement loan delinquencies rose from 0.89% to 0.91%.

RV loan delinquencies rose from 0.92% to 0.96%.

Open-end loans

Bank card delinquencies rose from 2.47% to 2.48%.

Home equity lines of credit delinquencies rose from 1.15% to 1.21%.

Non-card revolving loan delinquencies rose from 1.57% to 1.65%.

Related: Debt Collection Increasing Given Large Personal Debt Levels (2014) – Consumer and Real Estate Loan Delinquency Rates from 2001 to 2011 in the USA – Good News: Credit Card Delinquencies at 17 Year Low (2011) – Real Estate and Consumer Loan Delinquency Rates 1998-2009 – The USA Economy Needs to Reduce Personal and Government Debt (2009)

Since I am living in Malaysia now, I pay attention to Malaysia’s economy. There are many reasons to be positive but the large consumer and government debt in Malaysia is a serious concern. They do have many administrators that say the right things, the question is going to be whether those statement define policy action or if they are ignored.

Wahid Says Ringgit Too Weak as Growth Improves: Southeast Asia

India and Indonesia have experienced large stock market declines and currency devaluations recently. The Malaysian Ringgit has declines 10% against the US $ in the last 3 months. Malaysia is holding up ok, but is venerable as these international loses of confidence often sweep over countries (and move from country to country).

There is a real risk that the current account could slip into a deficit for the first time since the fourth quarter of 1997, Macquarie Group Ltd. analysts said in a report this month.

“We are aware of this situation and we are aware of some of the measures to be undertaken to make sure that Malaysia remains in a surplus position,” Abdul Wahid said, without elaborating on the steps. “It is still a surplus and we are managing it.”

The surplus is narrowing on increased overseas investment and property buying, higher imports for infrastructure projects, lower palm oil and rubber export prices and the acquisition of new aircraft by Malaysian Airline System Bhd., the minister said.

The main foreign exchange earner recently seems to be selling property, that isn’t a good way to be earning foreign currency (selling assets). It is ok to do this to some extent, but relying on large inflows this way is very risky (and self defeating over the long term if it is too large). Even though palm oil and rubber exports are declining a bit, I believe they are still strong sources of foreign currency so that is good.

Pitfalls in Retirement (pdf) is quite a good white paper from Meril Lynch, I strongly recommend it.

could safely spend 10% or more of their savings each year.

But, as explained below, the respondents most on target were the one in 10 who estimated sustainable spending rates to be 5% or less. This is significantly impacted by life expectancy; if you have a much lower life expectancy due to retiring later or significant health issues perhaps you can spend more. But counting on this is very risky.

This is likely one of the top 5 most important things to know about saving for retirement (and just 10% of the population got the answer right). You need to know that you can safely spend 5%, or likely less, of your investment assets safely in retirement (without dramatically eating into your principle.

Chart showing retirement assets over time based on various spending levels, from the Merill Lynch paper.

The chart is actually quite good, the paper also includes another good example (which is helpful in showing how much things can be affected by somewhat small changes*). One piece of good news is they assume much larger expense rates than you need to experience if you choose well. They assume 1.3% in fees. You can reduce that by 100 basis points using Vanguard. They also have the portfolio split 50% in stocks (S&P 500) and 50% in bonds.

Several interesting points can be drawn from this data. One the real investment returns matter a great deal. A 4% withdrawal rate worked until the global credit crisis killed investment returns at which time the sustainability of that rate disappeared. A 5% withdrawal rate lasted nearly 30 years (but you can’t count on that at all, it depends on what happens with you investment returns).

Related: What Investing Return Projections to Use In Planning for Retirement – How Much Will I Need to Save for Retirement? – Saving for Retirement

Countries that can still be travelled on the cheap

If you’re keen to surf or lie on the beach you’re all set to have an adventure for peanuts. As long as you steer clear of tourist-trap resorts, you’ll struggle to spend more than $23.50 a day. Nourish your inner cheapskate and buy souvenirs away from the tourist areas; head to the central market in Denpasar or Ubud’s Pasar Sukowati.

…

Eastern Europe used to be dirt cheap back in the good old days of the Cold War. Now that peace has broken out, costs are on the up. Poland, though, is still at the inexpensive end: a daily budget of $29 will easily get you around the country.

Poland is a nation that’s been run over so many times by invading forces that it’s become bulletproof. Now this EU member is on the rise, so get in quick before the prices go up for good. Rural towns are picturesque and cheap to visit; tiny towns like Krasnystaw in the Lubelskie region are a miser’s wonderland.

…

If you’re looking for a scuba-diving destination where you can put your entire budget into going under, Honduras is the place to be. With sleeping budgets as low as $12 a night and meals available for even less you can really stretch out the funds.

Sitting pretty next door to the Caribbean Sea, you’ll have plenty of time to count your pennies as you sun yourself on the golden beaches. The developers haven’t invaded quite yet, but you’d better get in quick, before the good old days slip into the past.

After snorkelling and kayaking around Roatan’s West Beach, splurge on a visit to the Unesco-listed Archaeological Park of Copan; entry is $18.

Related: Great Time for a Vacation – Travel guide books – Traveling To Avoid USA Health Care Costs – Travel Photo blog

…

According to Sharpe, who is also the founder of Financial Engines, the typical 4% rule recommends that a retiree annually spend a fixed, real amount equal to 4% of his initial wealth, and rebalance the remainder of his money in a 60%-40% mix of stocks and bonds throughout a 30-year retirement period.

What’s more, he shows the price paid for funding what he calls “unspent surpluses and the overpayments made to purchase its spending policy.” According to Sharpe, a typical rule allocates 10%-20% of a retiree’s initial wealth to surpluses and an additional 2%-4% to overpayments.

…

The only problem with what academia knows to be right and what’s practical in the field — even by Sharpe’s own admission — is this: “Many practical issues remain to be addressed before advisers can hope to create individualized retirement financial plans that maximize expected utility for investors with diverse circumstances, other sources of income, and preferences,” Sharpe wrote in his paper.

…

Meanwhile, Stephen P. Utkus, a principal with the Vanguard Center for Retirement Research, agrees that the 4% rule is flawed. But he also notes, as did Sharpe, that there’s no practical mechanism to replace it with and that further research is required.

I think this is exactly right. The proper personal financial actions in this case are not easy. The 4% rule is far from perfect but it does give a general idea that is a decent quick snapshot. But you can’t rely on such a quick, overly simplified method. At the same time there are simple ideas that do work, such as saving money for retirement is necessary. The majority of people continue to fail to take the most basis steps to save money each year for retirement.

Related: Spending Guidelines in Retirement – How Much Will I Need to Save for Retirement? – Bogle on the Retirement Crisis

3. The payment ploy: A dealer might say, “We can get you into this car for only $389 a month.” Probably true, but how? In some cases, the dealer may have factored in a large down payment or stretched the term of the loan to 60 or 72 months. Focus on the price of the car rather than the monthly payment. Never answer the question, “How much can you pay each month?” Stick to saying, “I can afford to pay X dollars for the car.”

Some good advice. I bought my last car at CarMax which gave a good price and none of these tricks (I didn’t have a trade in – I donated it) and I paid cash. They offered a great deal on a Toyota Rav4 when I was looking. I believe, those that are interested in getting the very best deal and are skilled and able to defend themselves from the dealer can do better than CarMax. But I would bet most people would be much better off using CarMax.

Related: Manufacturing Cars in the USA – Avoiding Phone Fees – Actually Free Credit Report – How to Use Your Credit Card Properly

The government has stopped some of the worst abuses by credit card issuers however, those financial institutions are not without ways of continuing to take advantage of customers, Credit-Card Fees: the New Traps

…

Banks already are reaping more fees on overseas transactions. Not only are they raising foreign-exchange transaction fees—the cost customers pay for purchases made in foreign currencies—but they are expanding the definition of what qualifies as a foreign transaction.

In the past, people who made online purchases from foreign merchants, or who traveled to a country where the purchases are often in U.S. dollars such as the Bahamas, were generally immune from paying such fees. But Citi and Bank of America recently imposed their 3% foreign-transaction fees on all foreign transactions—even if that purchase is charged in U.S. dollars. Discover Financial Services also began charging a new 2% for foreign purchases last year.

…

And there are ways to avoid annual fees. Citigroup is alerting some customers that it is assessing a $60 annual fee on their cards. The cure for that is simple. If you spend $2,400 on the card in a 12-month period, the bank will refund the fee.

I’ll tell you a better way to avoid the abusive fees. Don’t deal with the large banks that the government bailed out. My credit union offers a credit card with no annual fee without any minimum spending requirements, and many others do as well.

Related: How to avoid getting ripped off by credit card companies – More Outrageous Credit Card Fees – Sneaky Credit Card Fees – USA Consumers Paying Down Debt –

Five consumer laws you really ought to know if you live in the United Kingdom.

…

Your iconic white MP3 player, the totemic centre of your life, breaks down precisely 366 days after you bought it. The large electronics firm that sold you the MP3 player says that because the one-year guarantee had elapsed, there’s nothing they can do to help you. You’ll just have to buy another one.

…

if the player has been lovingly treated and has still conked out that suggests something may have been wrong with it at the very beginning.

It works like this. For the first four-five weeks you have a “right of rejection” – if the item you’ve bought breaks down, you can demand a refund.

For the next six months, you are entitled to replacement or repair of the goods. It is up to the retailer to prove there was nothing wrong with it if they wish to get out of having to do the work. And then after six months, there is still a duty to replace or repair faulty goods, but the onus is on you, the consumer, to prove that there was something wrong.

And the key time span is six years. That’s how long goods may be covered by the Sale of Goods Act. It all depends on what “sufficiently durable” means. If a light bulb goes after 13 months, the consumer is not going to be overly gutted.

Extended warranties are general a very bad personal finance move. I never purchase them. Many companies push them on customers because of the large profit margin and because they don’t want to provide value to customers.

Related: 10 Things Your Bank Won’t Tell You – Ohio Acts to Protect Citizens from Payday Loan Practices – Save Money on Printing – Don’t Let the Credit Card Companies Play You for a Fool – Student Credit Cards

China’s economy continues to grow quickly. It looks as though that, along with the slump in US car sales, likely will lead to China taking the world sales lead for cars (I would imagine for the first time ever the USA has not held this title). China 2009 Vehicle Sales May Rise 28% on Stimulus:

China has boosted auto sales this year through tax cuts and subsidies as a part of a wider 4 trillion yuan ($586 billion) stimulus that has shielded the country from the worst of the global recession. U.S. sales have slumped 28 percent, pushing the old GM and Chrysler LLC into bankruptcy. Last year’s total was 13.2 million, compared with 9.4 million in China.

Partially due to the strong internal Chinese demand (and partially due to Chinese regulation) India actually exports more cars than China. 5 times as many cars are purchased in China as are bought in India.

Indian Car Exports Beat China’s

…

In contrast, China’s exports slumped 60 percent to 164,800 between January and July, according to government data. Vehicles produced in Thailand for export declined 43 percent to 263,768, according to the Thai Automotive Club.

South Korean exports dropped 31 percent to 1.12 million units, according to the Korea Automobile Manufacturers Association. Japan, the world’s largest automobile producer and exporter, shipped 1.77 million cars, trucks and buses.

Related: The Relative Economic Position of the USA is Likely to Decline – Manufacturing Cars in the USA – Rodgers on the US and Chinese Economies

One factor you must understand when evaluating economic data is that the data is far from straight forward. Even theoretically it is often confusing what something like “savings rate” should represent. And even if that were completely clear the ability to get data that accurately measures what is desired is often difficult if not impossible. Therefore most often there is plenty of question about economic conditions even when examining the best available data. Learning about these realities is important if you wish to be financially literate.

Bigger U.S. Savings Than Official Stats Suggest

A closer look, however, shows that Americans have tightened their belts more sharply than the numbers report. The reason? Official figures for personal spending include a lot of categories, such as Medicare outlays, that are not under the control of households. They also include items, such as education spending, that should be treated as investment in the future rather than current consumption.

After removing these spending categories from the data, let’s call what’s left “pocketbook” spending – the money that consumers actually lay out at retailers and other businesses. By this measure, Americans have cut consumption by $200 billion, or 3.1%, over the past year. This explains why the downturn has hit Main Street hard.

…

Finally, for technical reasons the BEA throws in some “spending” categories where no money actually changes hands. The biggest is “rent on owner-occupied housing,” the money that people supposedly pay themselves for living in their own homes. Despite the housing bust, this number rose by 2.6% over the past year, to $1.1 trillion.

…

A closer look at BEA numbers shows that Americans reduced spending by 3.1% in the past year, indicating that the savings rate has risen to 6.4%

He raises good issues to consider though I am not sure I agree 100% with his reasoning.

Related: The USA Should Reduce Personal and Government Debt – Financial Markets with Robert Shiller – Save Some of Each Raise – Over 500,000 Jobs Disappeared in November (2008)