Home prices drop for fourth straight quarter. Wow – that sounds bad.

Wow, that doesn’t sound bad. For comparison the NASDAQ index was down 1.6% today. In addition, always remember median prices are not as straight forward as it might seem. The mix of housing that sells changes between the periods being compared. Often (though maybe not this time) as the housing speculation subsides the mix of houses shifts as fewer expensive houses are bought which would tend to mean even if prices for identical houses stayed the same the median price (of houses actually sold) would decline.

There are real changes taking place in the real estate market but the big changes are increased inventories, increased mortgage defaults and a credit crunch – not declining prices. My prediction of price drops was as small as any almost any I saw over the last few years. And so far, the declines are even less than I thought we would see. The biggest factor for the depth of the pricing declines is going to be how many houses are forced into foreclosure (which is unfortunately possibly going to be high due to adjustable rate mortgages being adjusted up and requiring higher mortgage payments).

In the short term, the credit crunch is having an impact and that may increase if the jumbo loans (for those with significant down payment and good credit) continue to be hard to finance. But I don’t expect that to be the situation even 3 months from now – of course I could be wrong. The real estate situation (pricing, inventory…), as often is the case, is hugely impacted by the location. Some areas, like Arizona and Florida, are being hardest hit now.

Related: Real estate articles – Beginning of the End of Housing Bubble? (2004) – Homebuilders’ confidence at 16-year low – mortgage information

Housing inventory glut gets fatter

…

The wait for tenants may be a long one. It’s much harder to get a loan these days for all but the best borrowers. Borrowers, for the most part, now must put more money down, document their income and assets, have few dings against their credit worthiness and show that they can afford the payments. Those tightened lending restrictions eliminate potential buyers from the market, reducing demand even as more supply hits the listings due to big jumps in foreclosures and builders finishing up projects initiated before the slump took hold.

What does the current data show about the real estate market overall? Across the country in the last year the median price has actually increased slightly. It looks like the data for the calendar year 2007 will show a decline for about 2%. Some areas have been much harder hit with median prices dropping over 10% (Las Vegas, Florida, Phoenix…). Mortgages any of 1) questionable credit score 2) jumbo loan or to a lessor extent with little money down are becoming hard to come by. Foreclosures are increasing dramatically. Builders are having a great deal of difficulty selling new housing they have built.

Still the decline in median prices is far from as dramatic as many feel (there have been large changes in the market but it still has not lead to a crash in home values or even a noticeable decline in most places). The increasing supply of houses for sale will put pressure on housing prices to decline. But without a significant continued increase in foreclosures (which is possible but it is still difficult to predict how large an increase we will see) I still do not believe we will see dramatic price declines in most of the country. The possibility (of say declines of over 15% in a year or two) is much higher now than it was in the last couple of years.

Post from 2004 on the real estate bubble worries then – again prices would have to fall a great deal to fall below the prices in 2004 (possible but not very likely to happen in the coming years). The real estate problems are significant and pose a danger to the economy (they certainly are already decreasing economic growth) however that is much different than a crash in housing prices. And as bad as the credit markets have been and rising foreclosures, increased housing inventory the anticipated crash in prices has still not been seen nationwide – and I stand by my belief we won’t see it. Though I will admit less confidently than at any time so far – I would hedge my bet on this prediction at this point (if I actually had bet any money on that prediction – I have no desire to sell any of my 401k money invested in real estate, my rental property or my house).

Your credit score may change as FICO creators drop authorized users

But some Internet-based credit-repair firms have been using this to boost the credit scores of strangers with poor credit. The firms pay a person with an excellent credit score to add someone with a rocky record as an authorized user on a card for a few months. The authorized user doesn’t ever use the plastic. Instead, he or she gets the benefit of the account owner’s credit history, which can raise a weak score by a couple of hundred points.

…

Worse for some, the change will mean no FICO score at all. Fair Isaac estimates 1.5 million to 3 million consumers will no longer have enough information in their credit report to be able to produce a FICO score. Among those most likely affected are young adults who have been added to their parents’ accounts.

Related: Example of Mortgage Payments Depending on Credit Score – Your FICO credit score explained

Sorry but that is a symptom of massive ignorance. Not knowing an incredible important aspect of your largest financial decision is like not know what days you are suppose to show up for work. There is a minimum amount of knowledge people should have that sign a mortgage. I think at least 34% of mortgage holders need to read this blog. Ok, I probably alienated all of them, so if that is the case then they should read some of the blogs we list in our blogroll.

There is a big problem in that logic – it could maybe make sense if you had good reason to believe rates will be lower in the future than when you took out the loan (but that is a very questionable). I don’t know why someone would think that in the last couple of years – the risks have been much better than rates would go up a few hundred basis points than down that much. Basically I can see someone that is very financially savvy using an adjustable mortgage to qualify and if they know they will move in a fairly short period…

Related: Learning About Mortgages – Mortgage Defaults: Latest Woe for Housing – How Not to Convert Equity – 30 year fixed Mortgage Rates

Comptroller Says Medicare Program Endangers Financial Stability:

…

Asked if he knows any politicians willing to raise taxes or cut back benefits, Walker says, “I don’t know politicians that like to raise taxes. I don’t know politicians that like to cut spending, but I think what we have to recognize is this is not just about numbers. We are mortgaging the future of our children and grandchildren at record rates, and that is not only an issue of fiscal irresponsibility, it’s an issue of immorality.”

Strong words and I agree, as stated in: Washington Paying Out Money it Doesn’t Have and USA Federal Debt Now $516,348 Per Household.

I am not exactly sure why but for some reason people seem very ignorant of the wealth distribution by age. The richest group by far are those over 65. There are several reasons for this including self preservation. Once you stop working you better have a large pool of capital or you will most likely have little income (you could have a great pension and no other savings but…). Another is that the “miracle” of compound interest. Those that actually saved enough for retirement often find their investments out-earning their spending thus wealth increasing yearly. This effect over time results in wealth increasing dramatically. Many of those that failed to save enough will have their savings dissolve very quickly thus leaving the inverse of a bell curve (a high number of wealthy and of poor and a lessor number in the middle). Social Security helps those that failed to save enough for retirement to slow the decline (and those that saved enough to become even wealthier even faster). The presence of large numbers of poor elderly I think is one reason so many are surprised that they are the richest age group.

I used to be surprised how few people know this – now I know, for those I talk to anyway, they are always surprised. This has several public policy impacts such as why do we have a huge “social security transfer system” (social security including medicare) to move money from the young to the old when the old are wealthier than the young? People see the 7.65% deducted from their check but the employer has to pay an equal amount to this transfer of wealth between the generations bringing the total to 15.3%.

It doesn’t make much sense to me to have those working at Wal-mart and McDonalds transfer 15.3% of the income from their labor to much wealthier people. Yes, paying something in I think is fair. But the system should be adjusted. One method I would use is to reduce (or eliminate) payments to the wealthy elderly (continuing the existing payments to the poor elderly is affordable so I see continuing those payments as good public policy) and reduce taxes on the working poor. Obviously others disagree so we transfer a large amount of money from those working at Wal-mart to those with hundreds of thousands in investments. I think this is wrong. I wish at least the facts would be known so that the decision is made with awareness of the facts.

…

The growing divide between the rich and poor in America is more generation gap than class conflict, according to a USA TODAY analysis of federal government data. The rich are getting richer, but what’s received little attention is who these rich people are. Overwhelmingly, they’re older folks. Nearly all additional wealth created in the USA since 1989 has gone to people 55 and older, according to Federal Reserve data. Wealth has doubled since 1989 in households headed by older Americans.

…

The implications are far-reaching and can turn conventional wisdom on its head. Social Security and Medicare increasingly are functioning as a transfer of money from less affluent young people to much wealthier older people.

Wow, I don’t recall seeing publications actually point out this fact very often. Good for the USA Today.

Read more

I am not even expecting good customer service but how about just the absence of customer hostility. The latest from Discover Card. I still have not received the money they said they would send (waiting more than a month now) – this is the amount they overcharged my bank (after they had already been told the charges were invalid. I guess it is acceptable to charge me for charges they knew were invalid?). But heck even accepting that, how about paying that money back as they said they would.

Amazingly they did send me a “bill” [with a balance they owe me instead of me owing them so it is not really a bill in the sense of money I owe them] for the account they said didn’t exist which was the reason they claimed that they could not pay the cash back bonus they promised. If people didn’t expect credit card companies to provide outrageously bad customer service wouldn’t this be seen as shockingly bad – so much so that certainly no company would tolerate it if it was brought to their attention. Well, we have evidence that such a thought is not true when dealing with Discover Card.

So according to Discover they don’t owe the money on the cash back bonus they promised because the account is closed. Yet they send me a bill (with a balance owed to me but it is exactly like the bill I would get from them each month including the cashback bonus section where instead of listing the amount they promised to pay me they list $0) that has an new account number on it. Paying what they promised in cash back bonus doesn’t seem like it would be hard (and frankly I can’t imagine not paying it in this circumstance can be acceptable according to the rules but who has the time to try and fight with them). And they don’t send the money that even they agree they owe, but instead just send a bill? What are they thinking?

As I said in a previous post if Discover Card pays the money they owe I will add an equal amount of my own money and lend that amount through Kiva (a charity that arranges loans from individuals to those in need worldwide on the micro-lending model). And I will either continue to roll those loans over for at least 10 years or I will donate the entire amount to a micro-lending charity (if for example Kiva shuts down or I decide that they are not doing a good job or whatever).

Read more

The merger condition required they offer the price point for 2.5 years. Unfortunately it appears it didn’t require that AT&T actually tell anyone about it.

So you can get discount DSL, if you live in the service area, and can figure out how to get the company to allow you to get the price they proposed to the court to bolster their case for merger approval. It sure would be nice if you could deal with companies that didn’t seem to have teams of lawyers kept busy trying to figure out how to say one thing while tricking customers out of as much money as possible. It seems to me we are getting less and less ethical. We just accept that companies are going to try and trick customers into paying as much as possible. My belief that you should just provide an honest service or product at a fair price seems to be some quaint old idea ![]() But since that seems to be the case you have to treat companies as though they are going to trick you in any way they can. Be careful out there.

But since that seems to be the case you have to treat companies as though they are going to trick you in any way they can. Be careful out there.

Related: Incredibly Bad Customer Service from Discover Card – Fake Checks That Make You Pay – Companies Claim to Value Customers

Jim Jubak makes a good case for why investing is safer overseas now.

…

And as I look ahead, I see few signs that the United States will put its financial ship into better trim and lower the country risk that comes with owning U.S. equities and bonds.

…

I think you need to compare markets one by one to look for those where investors, who tend to stick with the conventional wisdom until something whacks them over the head, have mispriced risk. The countries that I find particularly interesting as investment targets are those that have made the biggest strides in getting their houses in order.

He makes a good point. I have long advocated the benefits of international investing. And looking forward the potential for economic development (and investment gains) outside the USA are strong. As he says this does not mean abandoning the USA stock market but does mean thinking about increasing ownership of foreign stocks (probably using mutual funds though in our 10 stocks for 10 year portfolio we have 3 individual stocks: Toyota, Tesco (added in the December 2006 update), PetroChina and Templeton Dragon Fund [closed end mutual fund]).

Related: State of the nation? Broke – Our Only Hope: Retiring Later

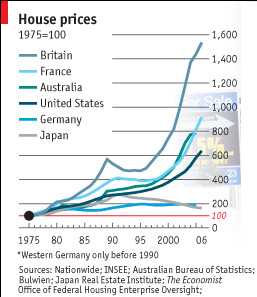

From 1975 to 2006 house prices in the UK increased 14 times. At 14 times that works out to about a 9% annual rate of return which is doesn’t sound nearly as impressive as a 14 fold increase to most people (I believe). The article does not mention if the chart is adjusted for inflation (a 9% return after inflation is incredibly good, a 9% return before factoring in inflation – which would reduce the rate of return – is good but reasonable) – my guess is that the chart is adjusted for inflation (meaning Britain’s owning real estate have been fortunate). Online calculator for annual rates of return over time.

Real estate rate of returns (when calculated on the total price) also underestimate the “real return” most investors experience because investors often only put down a portion of the investment. So the real rate of return is increased dramatically to the investor as a result of the the multiplier effect of buying on margin. Of course, real estate also has expense related to upkeep and the advantage of providing a place to live…

The graph (from the economist – see: Through the roof) shows other countries, USA: about 6 times, France 9 times… Remember these rates are averages for entire countries some areas in each country will have far exceeded these rates.

The graph could be a bit better if they didn’t make several of the colors almost the same.

Related: More Non Bubble Bursting in Housing – Europe and USA Housing Price Boom – How Not to Convert Equity – 30 year fixed Mortgage Rates