Scott Adams does a great job with Dilbert and he presents a simple, sound financial strategy in Dilbert and the Way of the Weasel, page 172, Everything you need to know about financial planning:

- Make a will.

- Pay off your credit cards.

- Get term life insurance if you have a family to support.

- Fund your 401(k) to the maximum.

- Fund your IRA to the maximum.

- Buy a house if you want to live in a house and you can afford it.

- Put six months’ expenses in a money market fund. [this was wise, given the currently very low money market rates I would use "high yield" bank savings account now, FDIC insured - John]

- Take whatever money is left over and invest 70% in a stock index fund and 30% in a bond fund through any discount broker, and never touch it until retirement.

- If any of this confuses you or you have something special going on (retirement, college planning, tax issues) hire a fee-based financial planner, not one who charges a percentage of your portfolio.

The Securities Investor Protection Corporation restores funds to investors with assets in the hands of bankrupt and otherwise financially troubled brokerage firms. The Securities Investor Protection Corporation was not chartered by Congress to combat fraud, but to return funds (with a $500,000 limit for securities and under that a $100,000 cap on cash) that you held in a covered account.

With the recent Madoff fraud case some may wonder about SIPC coverage. What SIPC would cover is cash fraudulently withdrawn from covered account (if I owned 100 shares of Google and they took my shares that is covered – as I understand it). What SIPC does not cover is investment losses. From my understanding Madoff funds suffered both these types of losses.

And I am not sure how the Ponzi scheme aspects would be seen. For example, I can’t imagine false claims from Mandoff about returns that never existed are covered. Therefore if you put in $100,000 10 years ago and were told it was now worth $400,000, I can’t image you would be covered for the $400,000 they told you it was worth – if that had just been a lie. And if your $100,000 from strictly a investing perspective (not counting money they fraudulently took to pay off other investors) was only worth $50,000 (it had actually lost value) then I think that would be the limit of your coverage. So if they had paid your $50,000 to someone else fraudulently you would be owed that. Figuring out what is covered seems like it could be very messy.

Read more

Fed Could Remake Credit Card Regulations

…

The proposal would also dictate how credit card companies should apply customers’ payments that exceed the minimum required each month. When different annual percentage rates apply to different balances on the same card, banks would be prohibited from applying the entire amount to the balance with the lowest rate. Many card issuers do that so that debts with the highest interest rates linger the longest, thereby costing the consumer more.

Industry officials have lobbied against the provisions, particularly the one restricting their ability to raise interest rates. They have warned that the changes would force them to withhold credit or raise interest rates because they won’t be able to manage their risk.

“If the industry cannot change the pricing for people whose credit deteriorates then they have to treat most credit-worthy customers the same as someone whose credit has deteriorated,” Yingling said. “What that means for most people is they’ll pay a higher interest rate.”

The government has been far to slow in prohibiting the abusive practices of credit card companies.

Related: How to Use Your Credit Card Responsibly – Avoid Getting Squeezed by Credit Card Companies - Legislation to Address the Worst Credit Card Fee Abuse – Maybe (Dec 2007) – Sneaky Credit Card Fees – Poor Customer Service: Discover Card

Recent market collapses have made it even more obvious how import proper retirement planning is. There are many aspects to this (this is a huge topic, see more posts on retirement planning). One good strategy is to put a portion of your portfolio in income producing stocks (there are all sorts of factors to consider when thinking about what percentage of your portfolio but 10-20% may be good once you are in retirement). They can provide income and can providing growing income over time (or the income may not grow over time – it depends on the companies success).

…

Strategy #3: Buy common stocks with solid dividends and a history of raising dividends for the long haul. That way you let time and compounding work for you. While you may be buying $1 per share in dividends today with stocks like these, you’re also buying, say, 8% annual increases in dividends. In 10 years, that turns a $1-a-share dividend into $2.16 a share in dividends.

3 of this picks are: Enbridge Energy Partners (EEP), dividend yield of 15.5%, dividend history; Energy Transfer Partners (ETP), 11.2%, dividend history; Rayonier (RYN), yielding 6.7%, dividend history.

Of course those dividends may not continue, these investments do have risk.

Related: S&P 500 Dividend Yield Tops Bond Yield: First Time Since 1958 –

Discounted Corporate Bonds Failing to Find Buying Support – Allocations Make A Big Difference

All you need is a broadband internet connection and you can Kiss your phone bill good-bye:

…

Replacing your phone service is, of course, just the start for Ooma. In some ways, calling is the Trojan horse to get the box in your house and then figure out other services to sell, like enhanced network security or kid-safe Web surfing.

One Year Later: Ooma by Michael Arrington

I just ordered mine from Amazon for $203. I have been using Vonage for awhile and have been considering canceling it for awhile (and just using my cell phone) but I currently have a limited cell phone plan (because unlike so many people, I don’t feel a need to talk to someone every single minute of the day). I normally just use the cell phone if I am meeting someone or traveling. Otherwise, just leave a message, I don’t need to speak to you right now.

Related: Save Money on Printing – Frugality Plus – Save Money on Food

Why the Germans just hate to spend, spend, spend

…

US, French and British officials puzzle over Germany’s refusal to tackle the recession head-on. German leaders, meanwhile, cannot see why their taxpayers’ money should go into encouraging precisely the kind of behaviour – reckless lending, careless borrowing and overconsumption – that precipitated the financial crisis.

I am with the Germans on this one. The people that want to find some more credit cards to run up don’t understand the problem. Until they come up with strong policies that admit we have been living beyond our means for decades and have to pay for this at some point and fashion a policy based on that understanding we are in danger. Yes another credit card can allow you to continue to live beyond your means, but it also puts you into even worse financial shape than you have already gotten yourself into. It is not a solution, it is an emergency to deal with the complete failure of yourself previously and without a plan to change it is just setting yourself up for a worse situation soon.

Related: How to Use Your Credit Card Responsibly – Have you Saved Your Emergency Fund Yet? – Can I Afford That? – Too Much Stuff

Diversification overrated? Not a chance by Jason Zweig

For anyone with a sustainable ability to identify the hottest investment of the moment, diversification is a mistake. But if you really believe you’ve got that ability, you’re not just mistaken. You need to be hauled off in a straitjacket to the Institute for the Treatment of Investment Insanity.

Exactly right. As we posted previously Warren Buffett’s diversification thoughts are similar

You have to remember when Warren Buffett says “professional and have confidence” he doesn’t really mean just what those words say. He mean if you are Charlie Munger, George Soros, Jimmy Rodgers and maybe 10 other people alive today (maybe I am too restrictive, maybe he would include 50 more people alive today, but I doubt it).

Related: Dilbert on Investing – investment risks – Curious Cat Investing and Economics Search Engine

Feds Rethink Rules on Retirement Savings

Among the possible changes: allowing taxpayers to delay taking required withdrawals from their individual retirement accounts, 401(k) plans and other similar accounts this year — or at least reducing the amount that must be withdrawn. Also under consideration are various ways to provide tax relief for people who already have made their required withdrawals for this year.

This is silly. Everyone in the situation of having to make a withdrawal has know about the requirement for years. My guess is this has been the law for over 20 years. Yes, the stock market is down. Yes, being forced to sell now would be bad. And how does providing “tax relief” to those who already made required withdrawals make any sense? Why not just have the treasury send checks to every American, who had a loss on an investment this year, equal to the amount of their loss? (By the way this is sarcasm – they should not really do that). These people have lost any sense of what investing, planning, responsibly… are.

First, knowing you have required withdrawals from your IRA, you should not hold those assets in stock (I suppose you could have significant cash assets outside your IRA and chose to just use the next option). Second, you can buy the stock outside your IRA at the same minute you sell them in the IRA. What is the big deal: the cost should be about $20 in stock commission for each stock – you save that much each time you fill up your gas tank lately (compared to prices this summer). All that not having to withdraw funds does is let those wealthy enough not to need a small amount of their IRA or 401(k) savings by the time they are 70 1/2 to keep deferring taxes on their investment gains.

Therein lies one of the major problems. This year’s distributions are based on Dec. 31, 2007, levels — a time when market prices generally were far above today’s deeply depressed values. As a result, “millions of Americans are forced to withdraw larger-than-anticipated amounts from already-depleted retirement funds,” says David Certner, legislative policy director at AARP, an advocacy group that represents nearly 40 million older Americans.

What kind of 1984 newspeak is this? I mean this is absolutely ridicules. You have to withdraw the exact amount you knew on January 1st 2008. Nothing about that has changed in almost a year. How can the Wall Street Journal report this without pointing out the completely false claim.

Read more

For me, giving back to others is part of my personal financial plan. As I have said most people that are actually able to read this are financially much better off than billions of other people today. At least they have the potential to be if they don’t chose to live beyond their means. Here are some of the ways I give back to others.

Kiva is a wonderful organization and particularly well suited to discuss because they do a great job of using the internet to make the experience rewarding for people looking to help – as I have mentioned before: Using Capitalism to Make a Better World. One of my goals for this blog is to increase the number of readers participating in Kiva – see current Curious Cat Kivans. I have also created a lending team on Kiva. Kiva added a feature that allows people to connect online. When you make a loan you may link you loan to a group.

I actually give more to Trickle Up (even though I write about Kiva much more). I have been giving to them for a long time. They appeal to my same desire to help people help themselves. I believe in the power of capitalism and people to provide long term increases in standards of living. I love the idea of providing support that grows over time. I like investing and reaping the rewards myself later (with investment I make for myself). But I also like to do that with my gifts. I would like to be able to provide opportunities to many people and have many of them take advantage of that to build a better life for themselves, their families and their children.

The photo shows Frew Wube, Haimanot and Melkan (brother and two sisters), an entrepreneur that received a grant from Trickle up. Trickle Up provides grants to entrepreneur, similar to micro loans, except the entrepreneur does not have to pay back the grant. They are able to use the full funds to invest in their business and use all the income they are able to generate to increase their standard of living and re-invest in the business.

“I also save every month,” says Frew, who has over $40 stored in a cooperative savings fund. The capital he has saved with other people in his group is used to provide loans to group members at a low interest rate. Frew, now able to access credit thanks to his Trickle Up clothing business, has taken progressively larger loans from the group, including his latest loan of $300 to start a candle business.

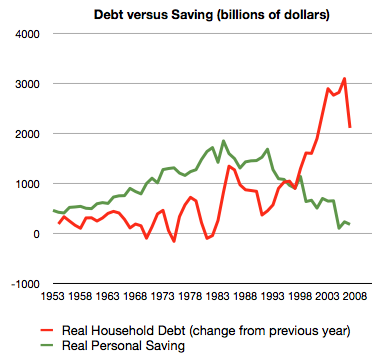

The whole sorry mess in one picture (including chart) by Philip Brewer

…

Starting back in about 2005, the American consumer reached the point that they could no longer service ever-increasing amounts of debt. That led to the housing bubble popping. The result is what you can see in the last datapoint on the graph–less new borrowing in 2007.

Related: $2,540,000,000,000 in USA Consumer Debt – Americans are Drowning in Debt – save an emergency fund – Financial Illiteracy Credit Trap – posts on saving money