I am a big fan of helping improve the economic lives of those in the world by harnessing appropriate technology and capitalism. It is wonderful what can be done to improve the lives of so many people with some intelligence and effort. This talk does a great job of showing how engineers thinking about the economic realities in the much of the world can design solutions to help. Without understanding the economic realities you cannot be effective.

Concludes Smith, “Something like 90% of the world’s resources creates products and technologies that serve only the wealthiest 10% of the worlds’ population. There’s a revolution afoot to promote R&D to get designers to work on technologies for the other 90%.”

Related: Nepalese Entrepreneur Success – Creating a World Without Poverty – Engineering a Better World: Bike Corn-Sheller – High School Inventor Teams @ MIT – Smokeless Stove Uses 80% Less Fuel

US living standards in jeopardy by James Jubak

…

the difference would get larger each year as the two rates were compounded. After 10 years at 2.3% growth, the U.S. economy would grow from $14.4 trillion in the third quarter of 2008 to $18.1 trillion, after accounting for inflation. At 3%, however, the U.S. economy would reach $19.4 trillion in gross domestic product.

…

The official unemployment rate hit 7.2% in December. Factor in part-time workers who would like to work full time and discouraged people who have stopped looking for work, and the real rate is more like 13.5%.

Some of those people won’t go back to work even when this recession is over because the relatively meager safety net supporting the unemployed in the United States will have given way beneath them. They will have suffered so much personal and family damage that they will never regain their full pre-recession productivity.

Related: Bad News on Jobs – The Economy is in Serious Trouble – Why Investing is Safer Overseas

How Should Parents Teach Teens About Credit Cards? by Nancy Trejos

…

there are prepaid cards targeted specifically at teens, such as the Visa Buxx card. With such a card, Bellamkonda would be able to log in and monitor his daughter’s spending online

…

Bill Hardekopf, chief executive of LowCards.com, said parents should pull out their own credit card bills and talk their children through them. Explain the interest rate, minimum payments, grace period and finance charges. If they’ve had late fees or payment problems, they shouldn’t hide them. “Use these as teaching examples,” he said. “Getting a teenager a credit card while she lives in your home is a great teaching opportunity on finances.”

I agree it is wise to explain the use of credit cards to teenagers. I also agree it is wise to have them actually use their own card, assuming they aren’t unreasonably immature and have shown an understanding of personal finance.

Books: Money Sense for Kids – Growing Money: A Complete Investing Guide for Kids – The Motley Fool Investment Guide for Teens – Raising Financially Fit Kids – A Smart Girl’s Guide to Money: How to Make It, Save It, And Spend It

Related: Teaching Children About Money Matters – Student Credit Cards – Majoring in Credit Card Debt

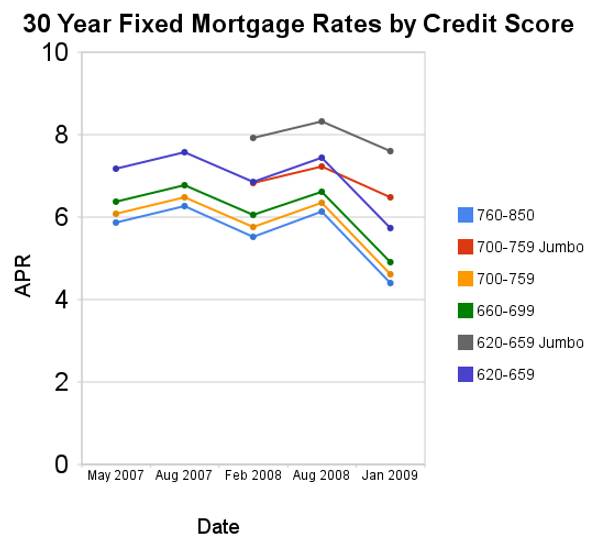

Since August of 2008 conforming mortgage rates are have declined a huge amount. Jumbo rates have fallen a large amount also, but much less (for example for a credit score of 700-759 the jumbo rates declined 73 basis points while the conventional rate declined 172 basis points.

For scores above 620, the APRs above assume a mortgage with 1 point and 80% Loan-to-Value Ratio. For scores below 620, these APRs assume a mortgage with 0 points and 60 to 80% Loan-to-Value Ratio. You can see, with these conditions the rate difference between a credit score of 660 and 800 is not large (remember this is with 20% down-payment) and has not changed much (the difference between the rates if fairly consistent).

Related: Low Mortgage Rates Not Available to Everyone – 30 Year Fixed Rate Mortgage Rate Data – Real Free Credit Report (in USA) – Jumbo Mortgage Shoppers Get Little Relief From Rates – posts on mortgages

Read more

The health care system in the USA is broken, as I have written about previously: USA Paying More for Health Care, International Health Care System Performance… One of the many problems created by the current system is ruined person finances for millions of people in the USA due to health care costs. The Rising Costs of Care And a Failing Economy Drive More Americans Into Medical Debt

…

Medical debt can quickly snowball. Consumers with unpaid bills can wind up in court defending themselves against lawsuits filed by doctors and hospitals, which typically charge the uninsured full price for care, without the hefty discounts negotiated by health plans. Debtors’ wages can be garnished, liens can be placed on their homes, and their future job and housing prospects torpedoed by bad credit ratings.

…

Unwilling to wait for federal action, a handful of states, most notably Massachusetts, have passed laws designed to expand health coverage or to protect medical debtors. An Illinois law passed last year caps rates that hospitals can charge the uninsured, while a New York statute bars foreclosures intended to pay off medical bills.

Purchasing health insurance against the risk of medical costs is critical to any financial plan. The concept (buying health insurance) is simple but securing that coverage is not as easy as knowing it is required for a sensible financial plan.

Related: Broken Health Care System: Self-Employed Insurance – Resources Focused on Improving the Health Care System – Excessive Health Care Costs

Consumer Credit Falls By Record Amount in November

This is good news. People need to stop spending money they don’t have. I understand perfectly well this means that spending will go down (which will likely lead to reduced economic output – though technically it doesn’t have to, a reduction in imported goods could more than offset the reduced spending and GDP would not decline). Living beyond your means is not a good thing. We should hope that consumer debt continues to decrease. If that means we have some suffering today to pay for living beyond our means for years the “fix” is not to continue to live beyond our means. The “fix” is to accept the consequences of past behavior and build a more sustainable economy now for the future.

Ideally this decrease can be someone gradual, abrupt changes in the economy often cause problems, but far too many economists and policy makers only care about today and the next 6 months. They have been living this way for decades. And it is not sustainable. Consumer debt levels in the USA are far too high. The UK has an even worse personal debt problem. They should come down. Reducing those levels is good for the individuals involved (they gain most of the benefit) and also for the health of the economy (though it does decrease the current economy a bit while making the foundation for future economy much stronger).

Read more

Madoff ‘victims’ do math, realize they profited

The issue came to the forefront this week as about 8,000 former Madoff clients began to receive letters inviting them to apply for up to $500,000 in aid from the Securities Investor Protection Corp. Lawyers for investors have been warning clients to do some tough math before they apply for any funds set aside for the victims, and figure out whether they were a winner or loser in the scheme.

Hundreds and maybe thousands of investors in Madoff’s funds have been withdrawing money from their accounts for many years. In many cases, those investors have withdrawn far more than their principal investment.

…

Jonathan Levitt, a New Jersey attorney who represents several former Madoff clients, said more than half of the victims who called his office looking for help have turned out to be people whose long-term profits exceeded their principal investment.

I discussed this aspect last month, the SPIC covers actual losses, not losses based upon false gains you didn’t have, I don’t think. So if you invested $100,000 and were told (falsely) it was worth $300,000 after years of gains you are not covered for $300,000. And I certainly hope the SPIC fund doesn’t payoff people who already had gains based on false accounting from Madoff.

This whole situation also points out the value of diversification. Diversification is important not just in asset classes (stocks, bonds, cash, real estate…) but in the accounts and companies with which you are dealing (I have always been a bit paranoid in this feeling, compared to others that think this level of diversification is not really needed but this is an example of the risks investments face that diversification can help manage). This is a very difficult situation for investors that had counted on assess they believed they had earned but in fact they had not.

Related: Bail us Out, say Madoff Victims – How to Protect Your Financial Health – Real Free Credit Report – identity theft links

According to the FDIC study of bank overdraft programs during 2007, 75% of banks automatically enrolled customers in automated overdraft programs (which charge high fees). By contrast, 95% of banks treated linked-account programs as opt-in programs, requiring that customers affirmatively request to have accounts link (which are normally do not charge customers high fees).

Fees assessed for linked-account and overdraft LOC programs were typically lower than for automated overdraft programs. Almost half of the banks with linked-account programs (48.9 percent) reported charging no explicit fees for the service. The most common fee associated with linked-account programs was a transfer fee; where charged, the median transfer fee was $5.

There really is no excuse (other than trying to gouge your “customers”) for these fee levels. Charging any money to just move money from a customers saving account to checking account is just making it obvious the bank doesn’t want to serve the bank wants to take money from you. The banks in the sample used by FDIC earned an estimated $1.97 billion in NSF-related fees in 2006, representing 74 percent of the $2.66 billion in service charges on deposit accounts reported by these banks.

A small fee when lending the customer money may be justified but the banks seem to just operate in order to have a big pool of people to catch them with big fees. The model seems to be if we get more “customers” we can catch more of them with one fee or another. It is not an honorable business model to try and catch your customers with huge fees for minor items.

Make sure you have a free linked-account overdraft protection that will tap your saving account if your checking account falls below 0. If they don’t have such a free program, choose a bank or credit union that does. Also an overdraft line of credit might be wise. If the fee is more than $10, go somewhere where they are not so greedy. You also will owe interest on your borrowings (probably a ludicrously high interest rate).

Related: Don’t Let the Credit Card Companies Play You for a Fool – 10 Things Your Bank Won’t Tell You – Hidden Credit Card Fees – FDIC Limit Raised to $250,000

$30.1 trillion in stock market valuation was wiped out last year – Journal of a Plague Year: Faith in Markets Cracks Under Losses:

…

Lehman Brothers Holdings Inc., with assets of $639 billion, filed the largest bankruptcy in U.S. history on Sept. 15. Its creditors may have lost as much $75 billion, the firm’s chief restructuring officer said.

Bear Stearns Cos. was taken over by JPMorgan Chase & Co. in March after a funding crisis triggered by losses from subprime- mortgage investments. Merrill Lynch & Co., facing a crisis of its own, sold itself to Charlotte, North Carolina-based Bank of America Corp. And the last two major investment banks, Goldman Sachs Group Inc. and Morgan Stanley, converted to bank holding companies and got capital injections from the U.S. government.

2008 was quite a memorable year in the markets. What the markets will do this year is hard to know. But the economy is likely to be very weak. Job losses will increase. If we are lucky the economy will be picking up by the end of the year. A huge problem is we have been living well beyond our means for decades. And now we are selling out even more of our children and grandchildren’s future to pay for the extravagance of those last few decades. How costly our credit-card-like financing of government bailouts is going to be is the most important issue I believe.

There is nothing wrong with spending money you saved for a raining day when that day comes. There is a big problem (for your future) taking our more credit cards to spend money you didn’t bother to save. You might have to do so, but the costs you are heaping on your future is very high (and for the economy overall many of those costs will be borne by children not yet born).

Related: The Economy is in Serious Trouble – Crisis May Push USA Federal Deficit to Above $1 Trillion for 2009 – What Should You Do With Your Government “Stimulus” Check? – Over 500,000 Jobs Disappeared in November

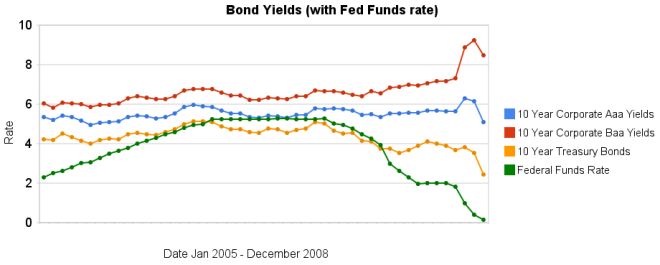

The recent reactions to the credit and financial crisis have been dramatic. The federal funds rate has been reduced to almost 0. The increase in the spread between government bonds and corporate bonds has been dramatic also. In the last 3 months the yields on Baa corporate bonds have increased significantly while treasury bond yields have decreased significantly. Aaa bond yields have decreased but not dramatically (57 basis points), well at least not compared to the other swings.

The spread between 10 year Aaa corporate bond yields and 10 year government bonds increased to 266 basis points. In January, 2008 the spread was 159 points. The larger the spread the more people demand in interest, to compensate for the increased risk. The spread between government bonds and Baa corporate bonds increased to 604 basis points, the spread was 280 basis point in January, and 362 basis points in September.

When looking for why mortgage rates have fallen so far recently look at the 10 year treasury bond rate (which has fallen 127 basis points in the last 3 months). The rate is far more closely correlated to mortgage rates than the federal funds rate is.

Data from the federal reserve – corporate Aaa – corporate Baa – ten year treasury – fed funds

Related: Corporate and Government Bond Rates Graph (Oct 2008) – Corporate and Government Bond Yields 2005-2008 (April 2008) – 30 Year Fixed Mortgage Rates versus the Fed Funds Rate – posts on interest rates – investing and economic charts