Welcome to the second edition of our investing and economics carnival.

- How Does the Current Crisis Compare to the Great Depression? by Price Fishback – “How does this compare to the Great Depression? We won’t know the final outcome of this recession for a while, but I can safely say that the current situation is nowhere near as bad as the situation during the 1930’s.”

- US GDP and imports by Matt Nolan – “Now, this doesn’t actually make sense as a measure to look at. Why? Well when we measure GDP we are interested in ‘domestic production’…”

- 100th Entrepreneur Loan by John Hunter – “Participating with Kiva is a great antidote to reading about the unethical ‘leaders’ taking huge sums to run their companies into the ground (or even just taking obscene sums to maintain their company). The opportunity to give real capitalists an chance at a better life is wonderful.”

- The Best 15 Financial iPhone Apps by David Weliver – “More than a dozen great financial apps for the iPhone make tracking and managing your personal finances on the go as easy as texting. Want to enlist your iPhone to help you get richer?”

- Bolster Your Emergency Fund In A Prolonged Crisis – “To prepare for the worst, we should picture an unemployed scenario and get serious about bulking up our emergency fund to meet at least six to eight months of expenses.”

- How to make money without a job and why you should – “There are two more advantages to alternative income besides diversification of income sources. First of all is the expansion of skills… You are learning something new, and making it that much more likely that you’ll be able to add further income streams…

- Five Low-Risk Stocks For Gen Y – “There are much better alternatives for the ultra-conservative Gen Y investors than money market accounts, Treasuries and CDs. A conservative strategy focusing on high quality, low risk dividend stocks should significantly out-perform the above investments, with very little incremental long-term risk.”

- 5 easy ways to save money and the environment – “Bottled water is a huge drain on our resources and are grossly overpriced. Reusable water bottles use fewer resources, save you money… Compact fluorescent light bulbs use 25% of the energy of standard incandescent bulbs and usually last 5 years or more…”

- Text Messaging is the Biggest Scam of the 21st Century – “The cost per GB of cable internet is $0.75… the cost per GB of cell phone data $6.00… the cost per GB of text messaging data is $800…”

I decided to add this investing and economics carnival after running the Curious Cat Management Management Improvement Carnival for several years. If you like these posts you may also be interested in the Invest Reddit where a community of those interested in investing submit and rate articles and blog posts.

Showing mortgage rates over the last 6 months. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate.

Showing mortgage rates over the last 6 months. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate.

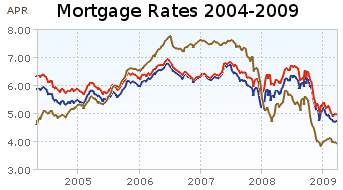

Showing mortgage rates over the last 5 years. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate. From Yahoo Finance, for conventional loans in Virginia.

Showing mortgage rates over the last 5 years. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate. From Yahoo Finance, for conventional loans in Virginia.

The 6 month chart shows that mortgage rates have been declining ever so slightly. Rates on a 1 year adjustable mortgage fell from 5.5 to 4% and have stayed near 4% for all of 2009. 30 and 15 year rates (15 year rates staying about 25 basis points cheaper) have declined from 6.5%, 6 months ago to about 5% at the start of the year and have moved around slightly since. This is while the yield 10 year government treasuries have been rising (normally 30 year fixed rate mortgages track moves in the 10 year government bond). The federal reserve has been buying bonds in order to push down the yield (and stimulate mortgage financing and other borrowing).

Mortgage rates certainly could fall further but the current rates are extremely attractive and I just locked in a mortgage refinance for myself. I am getting a 20 year fixed rate mortgage; I didn’t want to extend the mortgage period by getting another 30 year fixed rate mortgage. For me, the risk of increasing rates outweigh the benefits of picking up a bit lower rate given the current economic conditions. But I can certainly understand the decision to hold out a bit longer in the hopes of getting a better rate. If I had to guess I would say rates will be lower during the next 3 months, but I am not confident enough to hold off, and so I decided to move now.

Related: Mortgage Rates Falling on Fed Housing Focus – posts on mortgages – 30 Year Fixed Mortgage Rates and the Fed Funds Rate – Continued Large Spreads Between Corporate and Government Bond Yields – Lowest 30 Year Fixed Mortgage Rates in 37 Years –

Nonfarm payroll employment continued to decline in April, and the unemployment rate rose from 8.5 to 8.9 percent, the Bureau of Labor Statistics of the U.S. Department of Labor reported today. Since the recession began in December 2007, 5.7 million jobs have been lost. In April, job losses were large and widespread across nearly all major private-sector industries. Overall, private-sector employment fell by 611,000.

The number of unemployed persons increased by 563,000 to 13.7 million. Unemployment rates for April for adult men reached 9.4% and for adult women 7.1%. The number of long-term unemployed (those jobless for 27 weeks or more) increased by 498,000 to 3.7 million over the month and has risen by 2.4 million since the start of the recession in December 2007.

The civilian labor force participation rate rose in April to 65.8 percent, and the employment-population ratio was unchanged at 59.9 percent. The employment-population ratios for adult men and women showed little or no change over the month. However, since December 2007, the men’s ratio was down by 440 basis points, while the women’s ratio was down by 130 basis points. Since those that stop looking for work (retire or just stop actively looking) are not counted as unemployed the participation rate is a useful statistic to examine in conjunction with the unemployment rate.

Much of the commentary on the April job losses have been that the decrease in the number of job losses from previous months shows the economy is stabilizing. While it is true losing 611,000 jobs is better than losing 700,000 jobs, losing 611,000 is still very bad. The unemployment rate increased to 8.9% and long term unemployment is increasing drastically. This is hardly good economic news. It is true that there is hope that the economy is turning around, but the employment data we have so far is hardly positive (employment data is a lagging economic indicator so it is not surprising employment data does not recover before other signs point to improvement).

Related: Another 663,000 Jobs Lost in March in the USA – USA Unemployment Rate Rises to 8.1%, Highest Level Since 1983 – Over 500,000 Jobs Disappeared in November – What Do Unemployment Stats Mean?

The 2000–2002 bear market had three, with average gains of 21 per cent in the Dow Jones Industrials over 45 days.

The granddaddy of all bear markets, 1929 –1932, had six false alarms with an average gain of 47 per cent. And Japan’s ongoing bear saw the Nikkei rise by at least a third four times in its first four years with 10 more false dawns since then.

Bear markets typically end with a whimper rather than a bang, casting doubt on the latest recovery according to Hussman Econometrics, which analysed numerous US market bottoms and bear market rallies. With the exception of the 1987 crash, the month before the lowest point of a downturn saw a gradual descent.

I don’t put much money on the line trying to time the stock market. I thought the decline was overdone and I have found some things to buy. I am not convinced the current assent of the USA market especially means the bear market is over. If I had to sell stocks, I would be much happier to do it now than 3 months ago. That said, I am not selling anything or reducing my planned buying (401k buying).

Related: Financial Markets Continue Panicky Behavior (Oct 2008) – Trying to Beat the Market – Add to Your 401(k) and IRA – see my investing portfolio results

Consumer borrowing falls in March at fastest pace in over 18 years, Americans saving more

In dollar terms, consumer borrowing plunged by $11.1 billion. That’s the largest dollar amount on records dating to 1943, and more than three times the $3.5 billion drop that economists expected. The borrowing category that includes credit cards dropped 6.8 percent in March after a 12.1 percent plunge in February. The category that includes auto loans fell 4.2 percent after rising by 1.2 percent in February.

The Commerce Department last week said that the personal savings rate edged up to 4.2 percent in March, marking the first time in a decade that the savings rate has been above 4 percent for three straight months.

Good. Consumer debt is far to large and should be paid down. This is a start but a small start, but a much larger reduction in outstanding consumer debt is needed before we have reached a healthy level of debt. The continued improvement in that debt level signifies a stronger economy. Far too many financial journalists instead of pointing out the benefits of such improvement note that this reduces current consumption (and thus, effectively, will lower current GDP – compared to what it would be if we continued to spend beyond our means). You cannot spend money your don’t have forever.

Having more stuff in your house (along with an increased outstanding credit card balance) does not make you economically more successful. And the same holds true for the economy. Having more stuff sitting in people’s house and an increasing debt load is not the sign of a stronger economy (even if it is a route to a higher current GDP). Increased saving and reducing debt will strengthen the economy and improve our economic success over the long term.

Related: Will Americans Actually Save and Worsen the Recession? – Proper credit card use – Personal Saving and Personal Debt in the USA – Americans are Drowning in Debt – Buying Stuff to Feel Powerful

Each year Warren Buffett and Charlie Munger answer questions in front of crowds of tens of thousands of Berkshire Hathaway shareholders in Omaha, Nebraska. The question and answer sessions provide great wisdom on economics, investing and management. Here are some of the highlights I have found from the meeting yesterday.

Buffett, Munger praise Google’s ‘moat’

Berkshire’s Buffett Calls Wells Fargo ‘Fabulous’ Bank

The stock closed at $19.61 yesterday after falling below $9 in March. Buffett said he was speaking to a class the day the shares dropped that low and told students that, at that price, “If I had to put all of my net worth into stock, that would be the stock.”

Buffett, who has said he values lenders partly on their ability to acquire funds from depositors, told shareholders today that he’d “love” to buy the entire bank and is unable to do so because Berkshire wouldn’t get permission from regulators.

But he warned that efforts such as the Treasury’s $700 billion Troubled Asset Relief Program and the $787 billion fiscal stimulus plan passed this year by Congress will have to be paid for, one way or another. And with political leaders showing little inclination to raise taxes, one sure way to pay for excess spending is to inflate the value of the currency, Buffett said. The biggest losers in a surge of inflation, he added, would include holders of bonds and other fixed-income assets.

…

“Government does need to step in,” Buffett said, referring to the 6% contraction of the U.S. economy in the fourth quarter of 2008 and the first quarter of 2009.

That’s not to say he is pleased with the earmarks Congress has attached to some of the rescue legislation. Inevitably, Buffett said, when big organizations turn massive resources on a problem, “there’s a fair amount of slop.”

Related: Berkshire Hathaway Annual Meeting 2008 – Warren Buffett’s Letter to Shareholders 2009 – Great Advice from Warren Buffett – Warren Buffett’s 2004 Annual Report

Read more

U.S. Gas Fields Go From Bust to Boom

…

Huge new fields also have been found in Texas, Arkansas and Pennsylvania. One industry-backed study estimates the U.S. has more than 2,200 trillion cubic feet of gas waiting to be pumped, enough to satisfy nearly 100 years of current U.S. natural-gas demand.

The discoveries have spurred energy experts and policy makers to start looking to natural gas in their pursuit of a wide range of goals: easing the impact of energy-price spikes, reducing dependence on foreign oil, lowering “greenhouse gas” emissions and speeding the transition to renewable fuels.

…

new technologies and a drilling boom have helped production rise 11% in the past two years. Now there’s a glut, which has driven prices down to a six-year low and prompted producers to temporarily cut back drilling and search for new demand.

The natural-gas discoveries come as oil has become harder to find and more expensive to produce. The U.S. is increasingly reliant on supplies imported from the Middle East and other politically unstable regions. In contrast, 98% of the natural gas consumed in the U.S. is produced in North America.

Related: Oil Consumption by Country – posts on energy economics – Forecasting Oil Prices – South Korea To Invest $22 Billion in Overseas Energy Projects – Wind Power Provided Over 1% of Global Electricity in 2007

First Quarter GDP 2009 in the USA was down 6.1%. This is after a revised 6.3% drop in fourth quarter of 2008 (preliminary fourth quarter report showed a 6.2% decline). Real exports of goods and services decreased 30% in the first quarter, compared with a decrease of 23.6% in the fourth. Real imports of goods and services decreased 34.1%, compared with a decrease of 17.5%.

The personal saving rate — saving as a percentage of disposable personal income — was 4.2% in the first quarter, compared with 3.2% in the fourth quarter of 2008.

The news certainly is nothing to be happy about. But the stock markets around the world were buoyed by the Federal Reserves positive words:

Although the economic outlook has improved modestly since the March meeting, partly reflecting some easing of financial market conditions, economic activity is likely to remain weak for a time. Nonetheless, the Committee continues to anticipate that policy actions to stabilize financial markets and institutions, fiscal and monetary stimulus, and market forces will contribute to a gradual resumption of sustainable economic growth in a context of price stability.

True, those words hardly sound like great news but the markets were quite happy.

Related: The Economy is in Serious Trouble (Nov 2008) – Warren Buffett Webcast on the Credit Crisis – Fed Continues Wall Street Welfare (March 2008) – Manufacturing Data – Accuracy Questions

Peet’s Coffee: In Africa, Brewing Good Works by Steve Hamm

…

Because of bad roads and delays at border crossings, it took 12 days for a truck with a container full of green coffee beans to travel 1,000 miles to the Kenyan port of Mombasa. The sea journey from Mombasa took nearly two months. Worse, when the shipment arrived in Oakland, Calif., in late February, a portion of the coffee was slightly damaged.

Moayyad traveled to Rwanda to cement relationships with farmer groups and gather stories about the farmers for use in marketing. With a videographer tagging along, she navigated molar-crunching roads in a four-wheel-drive pickup to remote villages and farms perched on hillsides high above Rwanda’s Lake Kivu. On the roadsides, children greeted the passing truck with an excited cry of “Abazungu [white people]!” Moayyad plans to post a journal of her travels on Peet’s Web site, aimed at the company’s most loyal customers, called Peetniks.

A good effort. Real world issues confront you when you take steps to build the capacity for capitalism to help people live better lives. We need more such efforts to help capitalists make better lives for themselves around the world.

Related: Bill Gates: Capitalism in the 21st Century – International Development Fair, The Human Factor – Helping Capitalism Create a Better World – Frontline Explores Kiva in Uganda

It seems to me the situation that lead to the current economic problems are due to the overthrown of the Glass-Steagal and other long time sensible regulation put in place to restrict economy wide destruction caused by a few large financial firms (well, that plus incredibly poor management by people that paid themselves many times more than anyone else and other factors – huge consumer debt…). But the most significant systemic problem was failure to regulate even close to sensibly. I have several posts on this topic on previously: Congress Eases Bank Laws, 1999 – Treasury Now (1987) Favors Creation of Huge Banks – Canadian Banks Avoid Failures Common Elsewhere and Greenspan Says He Was Wrong On Regulation.

Capitalism requires sensible regulation. Regulation is not a friction on capitalism it is a necessary component. Poor regulation is a friction that is waste that should be excised. Unfortunately that is a very challenging task and when you allow those with the most gold to set the rules it is no surprise you have them saying they should not be regulated but should be protected. The failure of financial regulations do show the very obvious problem we have currently of those that donate huge amounts to politicians are granted favors that are paid for by the economy overall.

The widespread failure to regulate financial markets recently is almost certain to lead to this exact type of situation every time. Companies will over-leverage, take huge risks, take huge pay while times are good and just go bankrupt when times are bad. Think about how a bank makes money. They charge fees for things like: writing a loan, overdraft charges on your account, arranging financing (loan or stock sale)… They charge more for in interest than they pay. Some money there but really they are doing nothing special so they should not be able to charge too much. Even the ridicules fees companies pay (often those in the companies have arrangements to get personal special deals – allocations of IPO’s, jobs later…) for arranging stock sales do not have a systemic risk. Those risks should be very easy to manage sensible.

They speculate in currency markets, commodities markets, futures, derivatives… If you want a stable economy if you allow huge speculative investments to be assumed to such an extent they risk the economy you are in trouble. If you refused those risks to limited liability companies perhaps your limited regulation model might work. Where those profiting on products with negative economic externalities would personally go bankrupt prior to the losses becoming economically crippling. But I doubt even that would work. And we don’t have that now. We allow people to setup limited liability corporations, drain them of capital on speculation of potential value and then walk about with hundreds of millions of dollars if the company fails. And the negative externalities (due to huge leverage) are huge.

Regulation seems the obvious solution. And it works when applied. It wasn’t until the USA decided to abandon the financial system regulation and enforcement that the problems became systemic. And see the current Canadian banking system for what happens, even while the world economy is collapsing if you required banks to remain banks instead of massively leveraged speculators paying huge bonus to the executives based on their claims of profitability.

I agree trying to control risk is dangerous. There are however, very sensible measures to take. Do not allow huge financial companies to exist (we have laws on anti-trust, anti-competitive behavior…). Do not allow banks to speculate (more than a careful controlled regulated amount). Do not allow massive leverage of massive amounts of money. Do require audited financial records. Do require companies that want to speculate to be much smaller than regulated bank, and bank-like companies. Do elect politicians that will appose allowing companies to undertake systemic risks to the economy for short term financial gains.

We continue to elect politicians that provide large favors to those giving them money at the expense and risk to the rest of us. Therefore we are bringing this upon ourselves. When we chose to stop supporting politicians that behave in that way then we will get different behavior. Until that point it will continue. We don’t seems to be in any mood to change what we have been doing.

Comments on Note to Regulators: Beware the Montana Paradox

Related: More on Failed Banking Executives – more posts on regulation in capitalist economies – Credit Crisis the Result of Planned Looting of the World Economy – Bad Behavior