I posted before on how universities seek profits instead of helping students develop good financial literacy and habits. Here are some tips on how you should use your credit card. College Credit-Card Hustle

Using state public disclosure laws, Business Week has obtained more than two dozen confidential contracts between major schools and card-issuing banks keen to sign up undergraduates with mounting expenses for tuition, books, and travel. In some instances, universities and alumni groups receive larger payments from the banks if students use their school-branded cards more frequently.

The growing financial alliance between schools and banks raises questions about whether universities are encouraging students to incur additional high-interest debt at a time when many young people graduate from college owing tens of thousands of dollars.

…

Universities rarely negotiate favorable terms for their students, according to people familiar with the practice. On the contrary, some schools and booster groups entice undergraduates to sign up for cards with low initial interest rates that are soon replaced by steep double-digit rates.

Schools (and if some try to play legal games about alumni associations being separate, I don’t accept that) should fully disclose exactly what they are doing. I know they can make all sorts of excuses about why being open and honest is not right for them. Well, I think it is easy to predict they will be selling out their students and hiding that fact (if they must be open about what they are doing they will avoid some of the most egregious behavior because they know there will be consequences if they obviously sell out students). And, now Business Week has evidence that many are.

If a school is not open and honest about the deals they are making just assume they are selling out the students for their own gain. I can’t really see why we would want to support such behavior and I would encourage us not to.

Read more

Many Retirees Face Prospect of Outliving Savings, Study Says

…

Middle-income Americans entering retirement now will have to reduce their standard of living by an average of 24 percent to minimize their chances of outliving their financial assets, the study found. Workers seven years from retirement will have to cut their spending by even more — 37 percent.

This is one more study pointing out how many people are failing to take the most basic steps to manage their finances. Saving for Retirement is not very complicated. The details can get a bit complex but some of it is really basic like saving at least 5-15% of your earnings each year (or more if you fall behind) in tax differed savings accounts (IRA, 401(k)…). Many people just choose to sacrifice their future to buy more toys today.

There are different strategies but the minimum you should be doing (in the USA where social security will provide a portion of retirement savings) is saving, in a 401k, IRA or something similar: 5% in your 20s, 8% in 30s, 10% in your 40s, 11% in your 50s, 12% in your 60s. If you save more earlier you may be able to save less later. And if you fall behind you will have to save more. To retire earlier, than say 68 (today, or say 70 by 2020, and if you assume life expectancy rates will continue to increase you need to plan on working longer or saving more for a longer retirement), you should save more.

Read more

I commented on, WaMu Free Checking: The High 3.3% APY May Be Worth A Look, yesterday:

I agree it is worth considering. It has FDIC insurance. But the bank is not very stable. The stock price, for example, was above 40 in the last year. It is below 5 now. But as long as your entire deposit is covered by FDIC you are in safe (though if a bank goes under – not that likely – there can be a delay in getting your money). Normally a bank’s assets would be bought out by another bank.

And today I read of the second largest bank failure in the history of the USA, IndyMac Bank seized by federal regulators:

Regulators said depositors would have no access to banking services online and by telephone this weekend, but could continue to use ATMs, debit cards and checks. Online banking and phone banking services are to resume operations Monday.

Federal authorities said based on a preliminary analysis, the takeover of IndyMac would cost the FDIC between $4 billion and $8 billion.

It is important to make sure your deposits are FDIC insured (in the USA), and to know the limits of the coverage.

FDIC Failed Bank Information Information for IndyMac Bank, F.S.B., Pasadena, CA

IndyMac was a huge mortgage focused bank. Their stock price had fallen from a high of nearly $30 in the last year to below $5 in April, $2 in May and $1 in June. It is a very good thing we have the FDIC.

Related: Credit Crisis (August 2007) – Credit Crisis Continues – Homes Entering Foreclosure at Record

Failing to save is a huge problem in the USA. Spending money you don’t have (taking on personal debt) and not even having emergency savings and retirement savings lead to failed financial futures. Even though those in the USA today are among the richest people ever to live many still seem to have trouble saving. Here is a simple tip to improve that result for yourself.

Anytime you get a raise split the raise between savings, paying off debt (if you have any non-mortgage debt), and increasing the amount you have to spend. I think too many people think financial success is much more complicated than it is. Doing simple things like this (and some of the other things, mentioned in this blog) will help most people do much better than they have been doing.

There are lots of ways to spend money. And many people find ways to spend all or more than all (credit card debt, personal loans…) they have which are sure ways to a failed financial future. So anytime you get a raise (a promotion, new job…) take a portion of that extra money and put it toward your financial future. The proportion can very but I would aim for at least 50% if you have any non-mortgage debt, don’t have a 6 month emergency fund, or are behind in saving for retirement, a house…

Exactly how you calculate if you are behind, I will address in a future post (or you can look around for more information). By taking this fairly simple action you will be setting yourself up for a successful financial future instead of finding yourself falling behind, as so many do. And then when things go badly, as they most likely will sometime during your life, you will have built up a financial position to draw on. Instead of, as so many do now, find that you were living beyond your means when things were going well – which it doesn’t take a genius to see will lead to serious problems when things take a turn for the worse.

So lets say you take a new job and get a raise of $4,000 a year. Instead of spending $4,000 more just put $2,000 away (pay off debt, add to your retirement savings, add to savings for a house, add to your emergency fund…). Then you get a promotion of another $3,000, increase your spending by $1,500 and save the rest. It is such a simple idea and just doing this you can find yourself in the top few percent of those making smart financial decisions. And if you get to the point that you are ahead in all your financial areas then you can take more of each raise you get (but most of the time you will have learned how valuable the extra saving are and figured out the extra toys really are not worth it). But if you want to, once you have created a successful financial life, you can choose to buy more toys.

Related: Retirement Savings Survey Results – Earn more, spend more, want more

There are external risks to your financial health. Many people ruin their financial health even before any external risk can, but lets say you are being responsible then what risks should you seek to protect yourself from?

| Risk | Strategy | Also |

|---|---|---|

| medical costs | health insurance | emergency fund, healthy lifestyle to reduce the likelihood of needing medical care |

| property losses (house damaged, car stolen, property damage…) | homeowners insurance, rental insurance | |

| job loss | emergency fund, unemployment insurance (provided by the government and paid for by the company in most cases – in the USA) | updating skills, maintain a career network, education, learning new skills |

| disability (which both damages your earning potential and often has medical care costs) | disability insurance, health insurance | social security disability insurance – in the USA |

| investment losses | sound investment portfolio and strategy (diversification, appropriate investments, adjusting investment strategy over time) | extra savings |

| having to pay damages caused to others | homeowners insurance often includes personal liability coverage (and car insurance often includes some coverage for damage you cause while driving). check and likely choose to pay for extra liability insurance – costs to add coverage is normally cheap. | |

| unexpected expenses | emergency fund | extra savings |

| loss of income of someone you rely on (spouse) | life insurance | extra savings |

Another protection is to be financially literate. You can risk your financial health by being fooled in spending money you should save, borrowing too much for your house, failing to buy the right insurance, using too much leverage, investing too much in high risk investments…

Related: credit card tips – personal finance tips – personal loan information

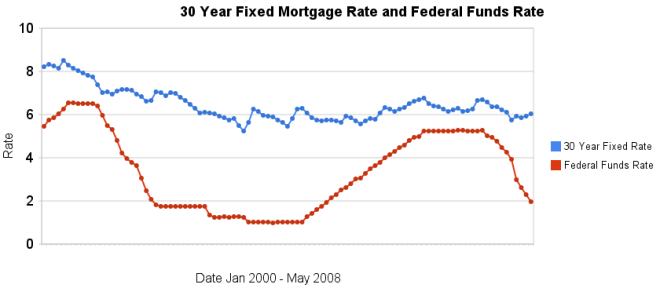

This year, the average discount rate has fallen every month while the average 30 year mortgage rate has climbed all but 1 month (a 5 basis point drop). In January, 2008 the discount rate averaged 3.94% and 30 year conventional fixed rate mortgages averaged 5.76%. In May, 2008 the discount rate had fallen to 1.98% (for a 196 basis point drop) and 30 year conventional fixed rates had risen to 6.04% (for a 28 basis point increase).

The chart shows the federal funds rate and the 30 year conventional fixed rate mortgage rate from January 2000 through May 2008 (for more details see: historical comparison of 30 year fixed mortgage rates and the federal funds rate).

Related: Affect of Fed Funds Rates Changes on Mortgage Rates – real estate articles – Bond Yields 2005-2008 – Jumbo and Regular Mortgage Rates By Credit Score

Read more

The recent drastic reductions again emphasize (once again) that changes in the federal funds rate are not correlated with changes in the 30 year fixed mortgage rate. In the last 4 months the discount rate has been reduced nearly 200 basis points, while 30 year fixed mortgage rates have fallen 18 basis points.

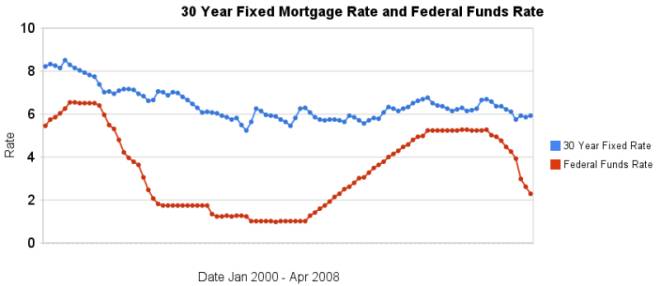

I have update my article showing the historical comparison of 30 year fixed mortgage rates and the federal funds rate. The chart shows the federal funds rate and the 30 year fixed rate mortgage rate from January 2000 through April 2008 (for more details see the article).

There is not a significant correlation between moves in federal funds rate and 30 year mortgage rates that can be used for those looking to determine short term (over a few days, weeks or months) moves in the 30 year fixed mortgage rates. For example if 30 year rates are at 6% and the federal reserve drops the federal funds rate 50 basis points that tells you little about what the 30 year rate will do. No matter how often those that should know better repeat the belief that there is such a correlation you can look at the actual data in the graph above to see that it is not the case.

Related: real estate articles – Affect of Fed Funds Rates Changes on Mortgage Rates – How Not to Convert Equity – more posts on financial literacy

Read more

At work people have been talking about the increasing prices of food and the price increases sure are noticeable to me. With the exception of gas, I have not heard discussion of inflation outside of a classroom, maybe ever, I can’t recall hearing it anyway. Egg prices are up 35 percent, with milk and bread not far behind

…

The crunch for American shoppers pales compared with the challenges faced by those in the developing world. Americans spend just 9.9 percent of household income on food, according to the Agriculture Department. Compare that with poor countries such as Ethiopia and Bangladesh, where it’s not uncommon for families to spend 70 percent.

Consumer Price Index Summary – March 2008:

Related: what is inflation risk? – Manufacturing Productivity – What Do Unemployment Stats Mean?

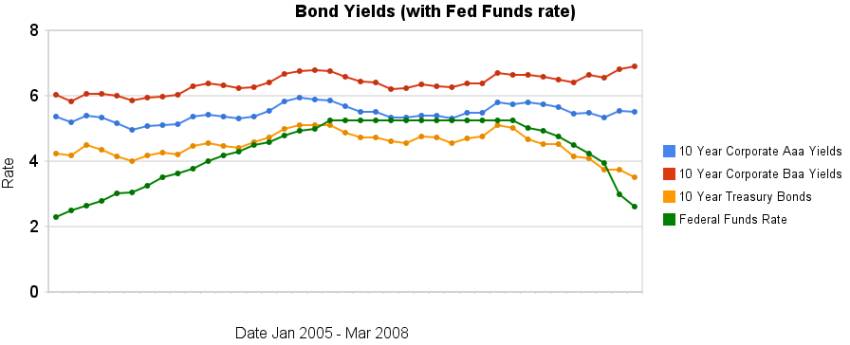

From January 2005 to July 2007 the Federal Funds Rate was steadily increased. The rate was held for a year. Since then the rate has been decreasing (dramatically, recently). As you can see from the chart, 10 year bond yields have been much less variable. The chart also shows 10 year corporate bond yields increasing in February and March when the federal funds rate fell well over 100 basis points.

Treasury bond yields are down but a huge part of the reason is a “flight to quality,” where investors are reluctant to hold other bonds (so they buy treasuries when they sell those bonds). Therefore other bond yields (and mortgage rates) are not decreasing. I guessed last month that the data “may well decrease some for both 10 year bonds once the March data is posted” which wasn’t the case. But I was right in “expect[ing] the spread between treasuries be larger than it was in January.”

Data from the federal reserve – corporate Aaa – corporate Baa – ten year treasury – fed funds

Related: 30 Year Fixed Mortgage Rates versus the Fed Funds Rate – After Tax Return on Municipal Bonds

Housing prices posted large declines over the last year. One important thing to keep in mind when looking at the recent results is how rare significant declines in housing prices have been. In general housing prices decline very little (less than 10% drops and normally less than 5%). Normally the turnover just decreases dramatically as people refuse to sell at lower prices and just stay in their house until prices recover. Housing Prices Post Record Declines:

Of those 20 metro areas, 17 posted their largest year-over-year declines ever. Ten of the 20 cities posted double-digit dips. The 10-city Case/Shiller index is down 13.6% year-over-year, the biggest drop since its launch in 1987

…

Prices in the Las Vegas metro area have plunged more than any other city, down 22.8% over the 12 months through February. Miami prices plummeted 21.7%. In Phoenix, they’ve fallen 20.8%. Of the 20 cities Case/Shiller tracks, only Charlotte, N.C. showed higher prices, up 1.5% over the 12-month period.

Other metro areas recorded only modest price declines, including Portland, Ore., down 2.0%, Seattle, off 2.7% and Dallas, 4.1%. In the nation’s largest city, New York, metro area prices dropped a modest 6.6%.

Related: Home Price Declines Exceeding 10% Seen for 20% of Housing Markets (Sep 2007) – How Not to Convert Equity – Housing Inventory Glut (Aug 2007) – Mortgage Defaults: Latest Woe for Housing (Feb 2007)