Much of personal finance is not amazingly complex once you take some time to lay out the basics. We have covered some important topics previously: tips on using credit cards, retirement saving, creating an emergency fund… One of the most critical factors is to insure yourself against possible catastrophic events.

Some personal finance mistakes can set you behind, say falling to save for retirement when you are 28 or cashing in your 401(k) when you switch jobs at 27. Those mistakes however are most often manageable. You just need to save more later. For health insurance the critical need is to protect yourself from huge costs.

Bankruptcies are a huge problem due to health costs. If you have done everything else right and have saved up say $150,000 in mutual funds (in addition to retirement savings and a house) at age 40 but have no health insurance there is little I can think of more likely to result in your losing that saving than a health crisis when you are without coverage (disability insurance is another critical personal finance need that I will discuss in another post and the another such risk – as is an uninsured home). The costs of health care are just too large for any but the richest to survive a major cost without either ruining an entire lifetime of smart financial moves or coming close.

There are certain things that cannot be compromised in your personal financial situation. Health coverage for significant costs is one of those. If you can afford a $5,000 (or higher) deductible that is fine. The critical need for health insurance is not the first $2,000 or $20,000 but the 2nd, 3rd, 4th… $100,000 bill. A bill for $2,000 you can’t afford is a challenge but a bill for $100,000 you can’t afford can ruin decades of smart and diligent financial moves.

Read more

Half of Gen X Doesn’t Expect to Retire

…

“They are earning money and paying into Social Security and yet they fear they may never see the payback,” said Moloney. “They feel they deserve it, but it looks like a financial black hole to them right now.”

The government certainly is failing to pay for future obligations today instead choosing to raise taxes on the future. But Social Security itself is actually in better shape than most think. We really do need to move out the benefit payment date (when it began projected life expectancy was almost the same as the date payments would start – which would mean moving the retirement date more than 15 years later, I believe). Going that far is not needed but it should be moved back. But really social security is in good shape for 30 years or more. First, it isn’t going to go from good shape to failed in a day. And second, they will make adjustments as they have in the past to make it work (the adjustment they made in the last 15 years helped a great deal so now they can just add some additional delays in when it starts paying out… and extend the good condition of Social Security without too much trouble).

Medicare is the huge problem. The country either needs to stop paying an extra 50-80% for health care than other countries do (and thus reduce the cost of Medicare liabilities) or massively cut benefits or massively increase taxes. Likely a combination of all 3.

Read more

Read a nice review of The Budget Deficit, the Current Account Deficit and the Saving Deficit:

- Tax incentives to encourage saving would likely also stimulate investment and lower both the budget deficit and the trade deficit.

- Reducing the budget deficit would reduce the vulnerability of the U.S. economy to foreign creditors; rising deficits could lead to foreigners dumping dollar assets, causing equities to decline, interest rates to spike and the dollar to plunge.

- Reducing the budget deficit doesn’t necessarily mean higher tax rates; marginal rate cuts reinforced by slower government spending growth would be ideal incentives.

Unfortunately, the recent tax “rebates” designed to stimulate the economy dealt a setback to budget discipline. Most people probably understand that. What they probably don’t understand is that the increased budget deficit will also tend to worsen our international balance of payments and weaken the dollar. The hip bone is connected to the thigh bone; so policymakers need to study these interconnected deficits. They need to borrow my boxes.

Lazy Portfolios update by Paul Farrell provides some examples of how to use index funds to manage your investments:

I think the article is a bit misleading in showing the out-performance of the S&P 500 index (during periods where the S&P 500 index does very well these portfolios will under-perform it). The out-performance shown in the article is largely due to the great performance of international markets recently. Still the strategy is well worth reading about. The strategy is based on using index funds from Vanguard (very well run mutual funds with very low fees). But don’t get tied into Vanguard, if they start to focus on lining their pockets by increasing your fees look for alternatives.

Overall, I give this concept high marks. Dollar cost average appropriate levels of money into such a strategy and you will give yourself a good chance at positive results.

My preference would be to include significant levels of international and developing stocks. For aggressive long term investing I like something like:

40% USA total stock market

15% Real Estate

25% international developed stock market index

20% developing stock market index

When aiming for more security and preserving capital (over growth) I favor something like:

30% USA total stock market

10% Real Estate

25% international developed stock market index

10% developing stock market index

10% short term bond index

15% money market

Of course all sorts of personal financial factors need to be considered for any specific person’s allocations.

Related: Allocating Retirement Account Assets – Why Investing is Safer Overseas – Saving for Retirement – 12 stocks for 10 years – what is a mutual fund?

In response to: What do you think? Should you discuss finances with your children?

…

We both waffle back and forth on these two perspectives and right now we’ve settled somewhere in between. Our children know we have debt, but don’t know the amount. They know I make pretty decent money, but don’t know how much. Our older boys pretty much know the details of our monthly expenses, such as the cable bill, phone bill, utility bills, etc. We’ve shared this with them to help them appreciate things a little more.

I definitely think talking about finances with children is important. I don’t have kids, but I was one ![]() I don’t think you need to get into exactly what the figures are to have valuable conversations. Far too many people become adults with far too poor an understanding of personal finance. Given how important managing money is today I think it is like hunter-gathers not teaching a kid how to hunt.

I don’t think you need to get into exactly what the figures are to have valuable conversations. Far too many people become adults with far too poor an understanding of personal finance. Given how important managing money is today I think it is like hunter-gathers not teaching a kid how to hunt.

Books: Money Sense for Kids – Growing Money: A Complete Investing Guide for Kids – The Motley Fool Investment Guide for Teens – Raising Financially Fit Kids – A Smart Girl’s Guide to Money: How to Make It, Save It, And Spend It

A few blog posts on teaching children about money: Personal Finance for Children and Pre-Teens – 5 Tips for Savvy Parents – Teach your teen the basics of money management

Related: Questions You Should Ask About Your Investments – Why Americans Are Going Broke – How Not to Convert Home Equity

The day the dream of global free- market capitalism died

The lobbies of Wall Street will, it is true, resist onerous regulation of capital requirements or liquidity, after this crisis is over. They may succeed. But, intellectually, their position is now untenable.

The intellectually depravity of such claims were obvious well before. Two problems make that truth less important. First, few actually believe in intellectual rigor any longer. Second, huge payments to politicians from those wishing to receive special favors from the government work (not very surprisingly). So given the lack of intellect and the alternative of just rewarding those that pay you huge sums of money it is no surprise politicians turned against capitalism and instead gave favors to a few that paid them well.

Maybe the latest huge bailout will change how things are done. I doubt it. New rules will be put in place. Plenty of people will pay politicians plenty of money to assure their methods of subverting the intent of those rules are allowed to continue. To change things you would need to vastly improve the intellectual rigor of decision making. That is unlikely, but if it happens it will be plenty obvious from how debate is carried out.

Read more

It has long been the case that home owners refuse to accept falling prices and choose to demand higher prices than the market demands in a falling market. Therefore when prices should fall (to find buyers) instead the sales decrease as buyers don’t decrease prices to a level buyers are willing to pay. Be It Ever So Illogical: Homeowners Who Won’t Cut the Price

Three years ago, when the real estate bubble was still inflating, this sort of standoff was the exception. It’s the norm today. Overall home sales have fallen a remarkable 33 percent since the summer of 2005. Home prices, on the other hand, continued to rise until 2006 and are now only 5 to 10 percent below where they were in mid-2005, according to various measures.

From the official US Federal Trade Commission site:

Viewing your credit report is an important step to financial security. You should review your credit reports annually (at least) to correct and any errors. Also doing so can be a tool to help you spot identity theft. The credit report site also has a large frequently asked question section with answers to questions like: What is a credit score? How do I request a “fraud alert” be placed on my file? Should I order all my credit reports at one time or space them out over 12 months? (I would suggest spreading the requests out during the year myself).

Reposting, original is from last January.

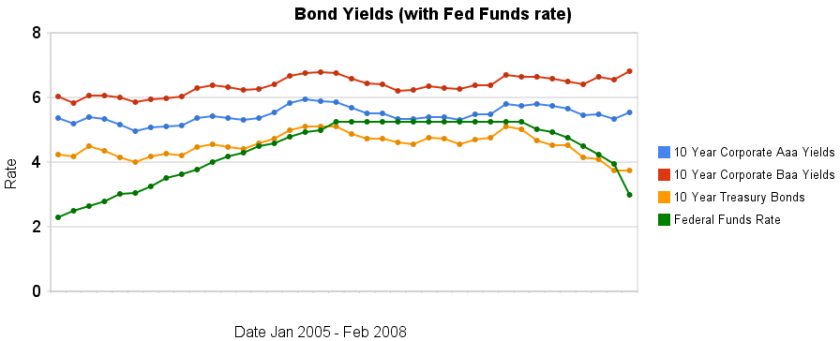

From January 2005 to July 2007 the Federal Funds Rate was steadily increased. The rate was held for a year. Since then the rate has been decreasing (dramatically, recently). As you can see from the chart, 10 year bond yields have been much less variable. The chart also shows 10 year corporate bond yields increasing in February when the federal funds rate fell 100 basis points.

Is the worst over, or just beginning?

…

If rates continue to fall, they could hit not only a new low for the year – the 10-year briefly touched 3.28% in January – but could come close to falling below the 3.07% level they hit in June 2003, which was a 45-year low at the time.

Treasury bond yields are down but a huge part of the reason is a “flight to quality,” where investors are reluctant to hold other bonds (so they buy treasuries when they sell those bonds). Therefore other bond yields (and mortgage rates) are not decreasing (the data in the chart is a bit old – the yields may well decrease some for both 10 year bonds once the March data is posted, though I would expect the spread between treasuries be larger than it was in January).

Data from the federal reserve – corporate Aaa – corporate Baa – ten year treasury – fed funds

Related: 30 Year Fixed Mortgage Rates versus the Fed Funds Rate – After Tax Return on Municipal Bonds

So lets say you have a 401(k) and are adding to it regularly, you own your house, you have no credit card debts, you are paying off your car loan and overall your financial house is in fairly good order. Still you keep hearing the news about credit crisis, mortgage meltdown, dollar depreciation… It is enough to make you nervous but what should you do?

Frankly very little in the macro economy has much impact on what is a smart long term strategy. Should you move your retirement money into a money market fund, because of the risks of stocks now? No. If you are good enough to time the market you are already amazingly rich (or will be soon). But either no one is able to do this or next to no one is. Occasionally you might get lucky and time things right but being able to consistently do so over 40 years is just not something that happens.

So what you should do now is what you should always do. Have cash savings. Pay off your mortgage (don’t over-leverage yourself – don’t take out equity just because you have some). Save for retirement. Have health insurance. Don’t take on credit card debt (or most other debt). Keep up your employment skills (learn new skills…). Diversify your investments (stocks, international stocks, real estate, cash…).

People often get careless when the overall economy is good. And so maybe you failed to do what you should have been doing then. But the right thing to do today is essentially the right thing to do always. For example, Americans are drowning in debt. They were also drowning in debt 3 years ago. That problem is the same. If you have too much debt you should fix that. Not because of all the fear today, but because to much debt is always bad. You should not take out too much debt in the first place and if you have to much you should fix it whether the economy is strong or weak.

Read more