So lets say you have a 401(k) and are adding to it regularly, you own your house, you have no credit card debts, you are paying off your car loan and overall your financial house is in fairly good order. Still you keep hearing the news about credit crisis, mortgage meltdown, dollar depreciation… It is enough to make you nervous but what should you do?

Frankly very little in the macro economy has much impact on what is a smart long term strategy. Should you move your retirement money into a money market fund, because of the risks of stocks now? No. If you are good enough to time the market you are already amazingly rich (or will be soon). But either no one is able to do this or next to no one is. Occasionally you might get lucky and time things right but being able to consistently do so over 40 years is just not something that happens.

So what you should do now is what you should always do. Have cash savings. Pay off your mortgage (don’t over-leverage yourself – don’t take out equity just because you have some). Save for retirement. Have health insurance. Don’t take on credit card debt (or most other debt). Keep up your employment skills (learn new skills…). Diversify your investments (stocks, international stocks, real estate, cash…).

People often get careless when the overall economy is good. And so maybe you failed to do what you should have been doing then. But the right thing to do today is essentially the right thing to do always. For example, Americans are drowning in debt. They were also drowning in debt 3 years ago. That problem is the same. If you have too much debt you should fix that. Not because of all the fear today, but because to much debt is always bad. You should not take out too much debt in the first place and if you have to much you should fix it whether the economy is strong or weak.

Read more

Ok the title is a bit of an misstatement but I am getting so tired of massive government transfers to the rich. Basically here is what has happened. People with tens and hundreds of millions of dollars didn’t want to be subject to pesky regulations just because capitalism requires it. So they paid their politicians to not regulate their investment activities. They paid their lawyers to evade the legal requirements that they couldn’t get their political friends to remove.

Largely what they did was take huge amounts for taking positions that risk the economy for personal gain. The investments have huge leverage and massive negative externalities to the economy. Any capitalist would know this is exactly what the government is suppose to protect the economy from. Unfortunately our politicians think capitalism is that whoever has the gold, therefore should make the rules. A sad state but not a surprise.

So then, the negative externalities begin taking effect and the government now seems to think that massive government intervention is a great thing. What a sad state of affairs.

What should happen now. That is hard to say.

But certainly with the amount of huge financial bailout the government has engaged in recently certainly they need to plan for this far in advance (it is obvious their preferred method of letting their friends take huge risks with the economy and pay themselves well while the risks work out requires huge bailouts very frequently).

You could, I suppose, decide everyone should pay to support a few thousand people being allowed take positions that have huge negative externalities (in risks to the economy) and pay themselves millions before those externalities become obvious and then bail them out when it doesn’t but that doesn’t seem like the best strategy to me. Though it is obviously the one we have chosen. This is one very non-partisan issue. They pretty much all support letting those that pay the politicians well, do whatever they want. And then support bailing them out if there are problems.

What should the government do in economic matters. Not at all hard to say. Politicians shouldn’t auction off the health of the economy to those that pay them the most money. Politicians should not allow companies to subvert the legal and tax system and be rewarded (just because those companies pay the politicians well and fly them to nice vacations…). The government should regulate negative externalities as capitalism requires to function properly.

But most of all the voters need to vote for those actions. As long as voters elect those that believe in corporate welfare this is the natural result.

Related: Why Pay Taxes or be Honest – Politicians Give Lobbyists Tax Breaks for Billion Dollar Private Equities Deals (not the politicians are given the deal makers cash loans) – Estate Tax Repeal (payoff to the rich) – Politicians Again Raising Taxes On Your Children

Read more

Great advice from Warren Buffett. He spoke to students at UTexas at Austin business school and one of the students, Dang Le, posted notes of the discussion online. The internet is great.

On diversification:

Great advice. Warren Buffett uses great concentration (little diversification) but you are not Warren Buffett.

…

Getting turned down by HBS [Harvard Business School] was one of the best things that could have happened to me, bad luck can turn out to be good.

…

We did an informal office survey by looking at the total tax footprint versus the total income. I earned 46 million and paid a tax rate of 17.5%. My rate was the lowest, the average was 33%, and my cleaning lady paid 40%. The system is tilted towards the rich. The Forbes 400 total net worth has gone from 220 billion to 1.54 trillion, an increase of 7-to-1. You see in legislature that there is lobbying carried on by the powerful over issues such as the estate tax and carried interest for private equity investments. We need to flatten income and payroll taxes, and those making under $30,000 shouldn’t be bothered.

It is hard to beat reading Warren Buffet’s ideas on investing and economics.

Related: Buffett on Taxes – The Berkshire Hathaway Meeting 2007 – Buffett’s 2006 Letter to Shareholders – Warren Buffett’s 2004 Annual Report – books on investing

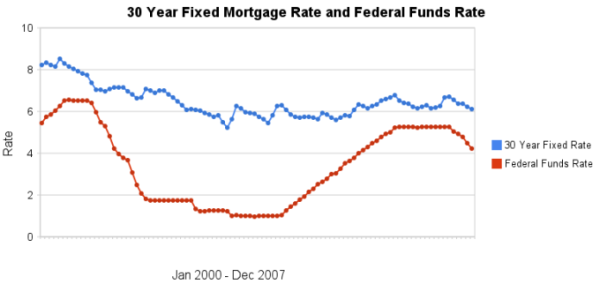

I have update my article showing the historical comparison of 30 year fixed mortgage rates and the federal funds rate. When deciding whether to lock in a rate for a 30 year fixed rate mortgage (when refinancing or buying a new home) some believe moves in the federal reserve discount rate will raise or lower that mortgage rate directly. This is not the case, in general. The effect of federal reserve discount rates on other mortgage rates (such as adjustable rate mortgages is not the same and can be predictably affected by fed fund rate moves).

The chart shows the federal funds rate and the 30 year fixed rate mortgage rate from January 2000 through December 2007 (for more details see the article).

There is not a significant correlation between moves in federal funds rate and 30 year mortgage rates that can be used for those looking to determine short term (over a few days, weeks or months) moves in the 30 year fixed mortgage rates. For example if 30 year rates are at 6% and the federal reserve drops the federal funds rate 50 basis points that tells you little about what the 30 year rate will do. No matter how often those that should know better repeat the belief that there is such a correlation you can look at the actual data in the graph above to see that it is not the case.

Read more

Here is updated data from the UN on manufacturing output by country. China continues to grow amazingly moving into second place for 2006. UN Data, in billions of current US dollars:

| Country | 1990 | 2000 | 2004 | 2005 | 2006 | |

|---|---|---|---|---|---|---|

| USA | 1,040 | 1,543 | 1,545 | 1,629 | 1,725 | |

| China | 143 | 484 | 788 | 939 | 1096 | |

| Japan | 808 | 1,033 | 962 | 954 | 929 | |

| Germany | 437 | 392 | 559 | 584 | 620 | |

| Italy | 240 | 206 | 295 | 291 | 313 | |

| United Kingdom | 207 | 230 | 283 | 283 | 308 | |

| France | 223 | 190 | 256 | 253 | 275 | |

| Brazil | 117 | 120 | 130 | 172 | 231 | |

| Korea | 65 | 134 | 173 | 199 | 216 | |

| Canada | 92 | 129 | 165 | 188 | 213 | |

| Additional countries of interest – not the next largest | ||||||

| Mexico | 50 | 107 | 111 | 122 | 136 | |

| India | 50 | 67 | 100 | 118 | 130 | |

| Indonesia | 29 | 46 | 72 | 79 | 103 | |

| Turkey | 33 | 38 | 75 | 92 | 100 | |

So yet again everyone in Washington DC wants to raise taxes on your children and grandchildren to spend money today. We might be going into a recession because the bubble of financing real estate led to people spending money they couldn’t pay back. So now home construction is decreasing, banks are having trouble meeting within capitalization requirement without huge inflows of capital from abroad, excess housing supply…

The government has been spending huge amounts of money it doesn’t have for a long time. So what great ideas do our leaders have: put more burden on the children and grandchildren to pay for our spending today. What a sad state of affairs. And almost no-one seems to question this behavior.

Is the idea that we would go into a recession so remote these leaders never imagined it could happen? No, of course they new it would happen. So what should a country, company, individual do if they know they have some expected event in the future they might want to spend money on? This isn’t really tricky. I would guess many 8 years olds understand the concept. You put the money in the piggy bank for when you will want to spend it.

If you decide to spend not only all the money you have but borrow huge amounts that will tax your future earnings to pay back your current spending that is your choice (as long as you can find someone to lend you money). But as many parents have told their kids you have to live with the decisions you make. You don’t get to spend your money today. Spend tomorrows money today. Spend your kids money today. And then when, tomorrow comes, just spend all that money all over again. How can a country allow leaders to so transparently tax the future of the country?

It is a sad state of affairs. The country chooses not to sent aside funds for obvious future needs. Then instead of accepting the hole they have dug for themselves decides to tax their children even more to continue the spendthrift ways. I think we not only need to have politicians actually read the bills before they vote (they refuse to pass such a law) they need to read about the ant and the grasshopper.

I have no problem with the country choosing to set aside funds to use when they want to try and stave off a recessions (to pay for tax cuts or more spending). I do have a problem with: running enormous deficits every year, raising taxes on our children and grandchildren year after year, and then deciding to raise taxes even more on the future when the obvious happens and perfectly predictable desired expenditures present themselves. The get another credit card school of financial management (that everyone in Washington DC seems to practice) is not workable for a country over the long term. As anyone that has used that strategy personally will tell you – it works for awhile but eventually there are serious consequences.

Read more

A house is where you live–not an investment

Very good point – as long as you fall into that category of living there until you die. True for some people but far from all. Also, even for those people, it is not a complete view of the financial situation.

A reverse mortgage will allow you to sell the house and get paid for the rest of the time you live there. So you can build up equity over 20,30,40 years and then take a reverse mortgage and get payments every month (based on your investing in your house). Reverse mortgages, like many financial tools, can be applied poorly and is I would guess unethical behavior related to them is fairly high (so be very careful!). If you think of such an option you need to do your research and actually understand what you are doing – you can’t afford to be like the many ignorant mortgagors. The AARP offers information on Reverse Mortgages.

Additionally, you lock in a large part of your housing cost (you still have maintenance and taxes but you do not have every increasing rent. Now ever increasing rent is not a certainty but for many it is very likely rent will go up on average over the long term. Ownership of your home removes the risk of being priced out of the area you want to live by increasing rental prices over time. You also lose the potential of benefiting if rent prices fall over time, but I would say the more valuable of those options is avoiding the risk of rising rental prices.

Related: How Not to Convert Equity – Housing Inventory Glut – articles on home ownership and real estate

Behind the Ever-Expanding American Dream House

Consider: Back in the 1950s and ’60s, people thought it was normal for a family to have one bathroom, or for two or three growing boys to share a bedroom. Well-off people summered in tiny beach cottages on Cape Cod or off the coast of California. Now, many of those cottages have been replaced with bigger houses. Six-room apartments in cities like New York or Chicago have been combined, because upper-middle-class people now think a six-room apartment is too small. Is it wealth? Is it greed? Or are there more subtle things going on?

This is extreme wealth. It is also part of the reason housing prices take an ever increasing multiple of median income. Basically people are buying two houses (not just one). Average square footage of single-family homes in the USA: 1950 – 983; 1970 – 1,500; 1990 – 2,080; 2004 – 2,349.

Related: mortgage terms defined – Trying to Keep up with the Jones – Too Much Stuff – Investing Search Engine

A Washington official dares to tell the truth

…

Walker: The present value of future unfunded liabilities for Medicare, Social Security and other plans is $53 trillion.

Walker: “You’re supposed to leave the country not just the way you found it, but better prepared for the future. The baby boom generation is failing on that.”

Walker: President Bush’s Medicare drug plan and the way it was sold to Congress and the public was “unconscionable.” The true, $8 trillion pricetag “was never calculated, disclosed or debated.”

Walker: The $9 trillion national debt is much more important than the budget deficit. Through the miracle of compound interest on the debt, he says, it will eat up more and more of the country’s resources.

Right. I keep posting on this because it is very important. To understand economics you need to understand the true shape of the economy. And to manage your investments you need to understand the great risk of a rising debt load (whether it is you personally or a country). Charge It to My Kids – USA Federal Debt Now $516,348 Per Household – Why Investing is Safer Overseas – Lobbyists Keep Tax Off Billion Dollar Private Equities Deals and On For Our Grandchildren – Broke Nation

I originally setup the 10 stocks for 10 years portfolio in April of 2005. At this time the stocks in the sleep well portfolio in order of returns -

| Stock | Current Return | % of sleep well portfolio now | % of the portfolio if I were buying today | |

|---|---|---|---|---|

| PetroChina – PTR | 298% | 11% | 7% | |

| Google – GOOG | 210% | 17% | 13% | |

| Amazon – AMZN | 173% | 7.5% | 7% | |

| Templeton Dragon Fund – TDF | 116% | 17% | 13% | |

| Cisco – CSCO | 67% | 6.5% | 8% | |

| Templeton Emerging Market Fund – EMF | 67% | 3.5% | 5% | |

| Toyota – TM | 48% | 7% | 10% | |

| Tesco – TSCDY | 25% | 0% | 10% | |

| Intel – INTC | 18% | 4% | 8% | |

| Yahoo – YHOO | -2% | 4% | 5% | |

| Pfizer – PFE | -9% | 5% | 8% | |

| Dell | -16% | 7% | 10% |

In order to track performance I setup a marketocracy portfolio but had to make some adjustment to comply with the diversification rules. In December of 2006 I announced a new 11 stocks for the next 10 years (9 are the same, I dropped First Data Corporation, which had split into 2 companies and added Tesco and Yahoo). Earlier this year I added Templeton Emerging Market Fund (EMF) and reduced the TDF portion. Tesco also pays a dividend which I am not including in the calculation – that is one reason marketocracy is so nice it keeps track of all those details for you.

I have orders in to sell some of the PTR and TDF if the prices rises a bit more. In the marketocracy portfolio I have several smaller positions. I do this to comply with marketocracy’s diversity rules – I also have about 8% in cash (they still won’t let me buy Tesco). Google, PetroChina and Amazon have had an incredible few months. I am getting a little tired of Yahoo’s failure to deliver. I also think Amazon’s price has gotten a bit ahead of the performance but I think the performance is great and the long term looks strong.

The current marketocracy calculated annualized rate or return (which excludes Tesco – reducing the return, and has a significant cash position reducing the return) is 20% (the S&P 500 annualized return for the period is 13.4% – in addition to the other reductions in the return, marketocracy subtracts the equivalent of 2% of assets annually to simulate management fees – as though the portfolio were a mutual fund). View the current marketocracy Sleep Well portfolio page.

Related: 12 Stocks for 10 Years Update (Jun 2007) – 10 Stocks for 10 Years Update (Feb 2007) – 10 Stocks for 10 Years Update (Dec 2005)