Failing to save is a huge problem in the USA. Spending money you don’t have (taking on personal debt) and not even having emergency savings and retirement savings lead to failed financial futures. Even though those in the USA today are among the richest people ever to live many still seem to have trouble saving. Here is a simple tip to improve that result for yourself.

Anytime you get a raise split the raise between savings, paying off debt (if you have any non-mortgage debt), and increasing the amount you have to spend. I think too many people think financial success is much more complicated than it is. Doing simple things like this (and some of the other things, mentioned in this blog) will help most people do much better than they have been doing.

There are lots of ways to spend money. And many people find ways to spend all or more than all (credit card debt, personal loans…) they have which are sure ways to a failed financial future. So anytime you get a raise (a promotion, new job…) take a portion of that extra money and put it toward your financial future. The proportion can very but I would aim for at least 50% if you have any non-mortgage debt, don’t have a 6 month emergency fund, or are behind in saving for retirement, a house…

Exactly how you calculate if you are behind, I will address in a future post (or you can look around for more information). By taking this fairly simple action you will be setting yourself up for a successful financial future instead of finding yourself falling behind, as so many do. And then when things go badly, as they most likely will sometime during your life, you will have built up a financial position to draw on. Instead of, as so many do now, find that you were living beyond your means when things were going well – which it doesn’t take a genius to see will lead to serious problems when things take a turn for the worse.

So lets say you take a new job and get a raise of $4,000 a year. Instead of spending $4,000 more just put $2,000 away (pay off debt, add to your retirement savings, add to savings for a house, add to your emergency fund…). Then you get a promotion of another $3,000, increase your spending by $1,500 and save the rest. It is such a simple idea and just doing this you can find yourself in the top few percent of those making smart financial decisions. And if you get to the point that you are ahead in all your financial areas then you can take more of each raise you get (but most of the time you will have learned how valuable the extra saving are and figured out the extra toys really are not worth it). But if you want to, once you have created a successful financial life, you can choose to buy more toys.

Related: Retirement Savings Survey Results – Earn more, spend more, want more

There are external risks to your financial health. Many people ruin their financial health even before any external risk can, but lets say you are being responsible then what risks should you seek to protect yourself from?

| Risk | Strategy | Also |

|---|---|---|

| medical costs | health insurance | emergency fund, healthy lifestyle to reduce the likelihood of needing medical care |

| property losses (house damaged, car stolen, property damage…) | homeowners insurance, rental insurance | |

| job loss | emergency fund, unemployment insurance (provided by the government and paid for by the company in most cases – in the USA) | updating skills, maintain a career network, education, learning new skills |

| disability (which both damages your earning potential and often has medical care costs) | disability insurance, health insurance | social security disability insurance – in the USA |

| investment losses | sound investment portfolio and strategy (diversification, appropriate investments, adjusting investment strategy over time) | extra savings |

| having to pay damages caused to others | homeowners insurance often includes personal liability coverage (and car insurance often includes some coverage for damage you cause while driving). check and likely choose to pay for extra liability insurance – costs to add coverage is normally cheap. | |

| unexpected expenses | emergency fund | extra savings |

| loss of income of someone you rely on (spouse) | life insurance | extra savings |

Another protection is to be financially literate. You can risk your financial health by being fooled in spending money you should save, borrowing too much for your house, failing to buy the right insurance, using too much leverage, investing too much in high risk investments…

Related: credit card tips – personal finance tips – personal loan information

Graduates should put off living large after college

The key, experts say, is a simple one: Live like a poor college student for a couple more years. While you’re doing that, you can pay off your debt, start a savings plan and embrace healthy habits that will serve you well for life.

This is exactly what I did. Outside of paying for college, extra living expenses in college were small. Just retaining the spending habit of college gets your personal finances off on a good start.

Patty Procrastinator lives a little better when she first gets out of college and doesn’t start saving in the 401(k) until she’s 32. From that point, she also saves $500 a month, her employer adds $250 a month, and she earns a 9% return — just like Sallie. But at age 65, Patty will have only $1.7 million. That decade of delay will cost Patty $2.4 million.

Incidentally, Sallie contributes from her own money just $60,000 more than Patty does. The rest of the difference comes from employer contributions and investment returns.

By immediately starting to save for retirement and other needs you create a great foundation for your finances. Start saving for a house, a new car, create an emergency fund… Then you can create a situation where the only loans you need to take are for a house and maybe a new car – avoiding credit card debt or other personal loans.

Related: Personal Finance Basics: Health Insurance – Initial Retirement Account Allocations – Why Americans Are Going Broke

The best method to avoid problems with debt collectors is to avoid debt problems (Create Your Cash Reserve – use your credit card responsibly – Buy less stuff). But if you do run into problems and get stuck dealing with debt collectors in addition to the financial trouble you may find yourself very frustrated and stressed. The Fair Debt Collection resource of the Federal Trade Commission provides useful information:

Debt collectors may not harass, oppress, or abuse you or any third parties they contact. For example, debt collectors may not:

- use threats of violence or harm

- publish a list of consumers who refuse to pay their debts (except to a credit bureau)

- use obscene or profane language; or repeatedly use the telephone to annoy someone

Debt collectors may not use any false or misleading statements when collecting a debt. For example, debt collectors may not:

- falsely imply that they are attorneys or government representatives

- falsely imply that you have committed a crime

- falsely represent that they operate or work for a credit bureau

- misrepresent the amount of your debt

- indicate that papers being sent to you are legal forms when they are not

- indicate that papers being sent to you are not legal forms when they are

Why is such a resource needed? Because many debt collectors have behaved unethically and illegally. To file a complaint use that link or call toll-free, 1-877-382-4357.

FTC 2008 Report on Fair Debt Collection Practices Act

Read more

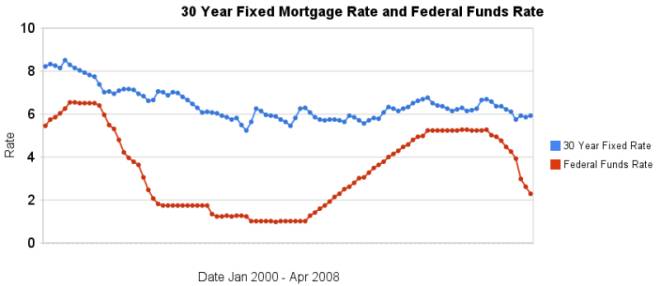

The recent drastic reductions again emphasize (once again) that changes in the federal funds rate are not correlated with changes in the 30 year fixed mortgage rate. In the last 4 months the discount rate has been reduced nearly 200 basis points, while 30 year fixed mortgage rates have fallen 18 basis points.

I have update my article showing the historical comparison of 30 year fixed mortgage rates and the federal funds rate. The chart shows the federal funds rate and the 30 year fixed rate mortgage rate from January 2000 through April 2008 (for more details see the article).

There is not a significant correlation between moves in federal funds rate and 30 year mortgage rates that can be used for those looking to determine short term (over a few days, weeks or months) moves in the 30 year fixed mortgage rates. For example if 30 year rates are at 6% and the federal reserve drops the federal funds rate 50 basis points that tells you little about what the 30 year rate will do. No matter how often those that should know better repeat the belief that there is such a correlation you can look at the actual data in the graph above to see that it is not the case.

Related: real estate articles – Affect of Fed Funds Rates Changes on Mortgage Rates – How Not to Convert Equity – more posts on financial literacy

Read more

Much of personal finance is not amazingly complex once you take some time to lay out the basics. We have covered some important topics previously: tips on using credit cards, retirement saving, creating an emergency fund… One of the most critical factors is to insure yourself against possible catastrophic events.

Some personal finance mistakes can set you behind, say falling to save for retirement when you are 28 or cashing in your 401(k) when you switch jobs at 27. Those mistakes however are most often manageable. You just need to save more later. For health insurance the critical need is to protect yourself from huge costs.

Bankruptcies are a huge problem due to health costs. If you have done everything else right and have saved up say $150,000 in mutual funds (in addition to retirement savings and a house) at age 40 but have no health insurance there is little I can think of more likely to result in your losing that saving than a health crisis when you are without coverage (disability insurance is another critical personal finance need that I will discuss in another post and the another such risk – as is an uninsured home). The costs of health care are just too large for any but the richest to survive a major cost without either ruining an entire lifetime of smart financial moves or coming close.

There are certain things that cannot be compromised in your personal financial situation. Health coverage for significant costs is one of those. If you can afford a $5,000 (or higher) deductible that is fine. The critical need for health insurance is not the first $2,000 or $20,000 but the 2nd, 3rd, 4th… $100,000 bill. A bill for $2,000 you can’t afford is a challenge but a bill for $100,000 you can’t afford can ruin decades of smart and diligent financial moves.

Read more

What Should You Do With a Check Out of the Blue?

The USA government is sending out checks to taxpayers in an effort to encourage spending which in turn will provide stimulus to the economy in the very short term. First, this is bad policy in my opinion. Second, if you support this policy the precondition is you run surpluses in order to pay for it when you want to carry out such a policy. They have not, instead they have run huge deficits. What they have chosen to do is spend huge amounts and have the taxes paid by the children and grandchildren of those the politicians are spending the money on today. I would support Keynesian government spending in a serious recession or depression – just not for a country already with enormous debts and in a very mild recession.

But ok, so the government chooses to spend your children’s taxes foolishly, what should you do now? This is very easy. Whatever is the wisest move for your personal financial situation for any windfall you receive, regardless of the source of that windfall. If all your savings needs are met there is nothing wrong with buying some toy. But most people need to pay off debt, build an emergency fund, save for retirement or something similar not get another toy. Of course would be nothing wrong with donating it Kiva, Trickle Up, the Concord Coalition or your favorite charity.

The politicians are acting like a 5 year old that wants a new toy. I can too get the new toy now :-O, Mommy you can use your credit card. So what if you already bought me so many toys you couldn’t afford by using your other credit cards and they won’t lend you any more money. Just get another one. Similar to how congress recently yet again increased the allowable federal debt limit to over $9,000,000,000,000.

The stimulus effect of spending is that if you actually purchase a new toy (say a TV), then the store needs to replace that TV so the factory makes another TV… The store, shipper, factory, supplier to the factory all pay staff to carry this out, those staff can buy new books, dishwasher… and the business may buy a new forklift or computer to keep up…

Read more

In response to: What do you think? Should you discuss finances with your children?

…

We both waffle back and forth on these two perspectives and right now we’ve settled somewhere in between. Our children know we have debt, but don’t know the amount. They know I make pretty decent money, but don’t know how much. Our older boys pretty much know the details of our monthly expenses, such as the cable bill, phone bill, utility bills, etc. We’ve shared this with them to help them appreciate things a little more.

I definitely think talking about finances with children is important. I don’t have kids, but I was one ![]() I don’t think you need to get into exactly what the figures are to have valuable conversations. Far too many people become adults with far too poor an understanding of personal finance. Given how important managing money is today I think it is like hunter-gathers not teaching a kid how to hunt.

I don’t think you need to get into exactly what the figures are to have valuable conversations. Far too many people become adults with far too poor an understanding of personal finance. Given how important managing money is today I think it is like hunter-gathers not teaching a kid how to hunt.

Books: Money Sense for Kids – Growing Money: A Complete Investing Guide for Kids – The Motley Fool Investment Guide for Teens – Raising Financially Fit Kids – A Smart Girl’s Guide to Money: How to Make It, Save It, And Spend It

A few blog posts on teaching children about money: Personal Finance for Children and Pre-Teens – 5 Tips for Savvy Parents – Teach your teen the basics of money management

Related: Questions You Should Ask About Your Investments – Why Americans Are Going Broke – How Not to Convert Home Equity

So lets say you have a 401(k) and are adding to it regularly, you own your house, you have no credit card debts, you are paying off your car loan and overall your financial house is in fairly good order. Still you keep hearing the news about credit crisis, mortgage meltdown, dollar depreciation… It is enough to make you nervous but what should you do?

Frankly very little in the macro economy has much impact on what is a smart long term strategy. Should you move your retirement money into a money market fund, because of the risks of stocks now? No. If you are good enough to time the market you are already amazingly rich (or will be soon). But either no one is able to do this or next to no one is. Occasionally you might get lucky and time things right but being able to consistently do so over 40 years is just not something that happens.

So what you should do now is what you should always do. Have cash savings. Pay off your mortgage (don’t over-leverage yourself – don’t take out equity just because you have some). Save for retirement. Have health insurance. Don’t take on credit card debt (or most other debt). Keep up your employment skills (learn new skills…). Diversify your investments (stocks, international stocks, real estate, cash…).

People often get careless when the overall economy is good. And so maybe you failed to do what you should have been doing then. But the right thing to do today is essentially the right thing to do always. For example, Americans are drowning in debt. They were also drowning in debt 3 years ago. That problem is the same. If you have too much debt you should fix that. Not because of all the fear today, but because to much debt is always bad. You should not take out too much debt in the first place and if you have to much you should fix it whether the economy is strong or weak.

Read more

The title of a recent article asks: Are you a sucker to invest in a 401(k)? The answer is an emphatic: No.

But what if instead you had bought that tax-efficient stock fund outside your plan? Wouldn’t your tax bill be lower? Yes, but that’s the wrong way to look at it. If you skip your 401(k) in favor of a taxable account, you must first shell out taxes on that $10,000, which leaves you with just $7,200 to invest (assuming the same 28% bracket).

Plus, over the next 20 years, you’ll have taxes on any dividends and gains the fund pays out. Even though you will get a lower 15% rate on your gains when you sell, you end up with $28,950, or about $4,600 less than with the 401(k). A tinier final tax bill can’t make up for having to pay taxes all along.

This is a very good short simple personal finance article. It explains an issue that might be tricky for some to understand. Those that read it can learn more about personal finance. And it has several points – some of which, I can imagine, might be hard for some to understand. But it does a good job of explaining things simply. And a few points, made well in the article, are often overlooked or under-appreciated:

tax rates will go up – we are passing higher taxes onto the future by not paying our bills now

the tax deferral is a huge benefit – often minimized when people discuss the benefits of IRAs

401(k) employer matches are another huge benefit

As I have said before, learning about personal finance is a long term effort. If you don’t understand everything in an article that is fine, over the years you want to learn more and more. Hopefully this is a useful step on that journey.

Related:

Roth IRAs a Smart bet for Younger Set – Saving for Retirement