Showing mortgage rates over the last 6 months. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate.

Showing mortgage rates over the last 6 months. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate.

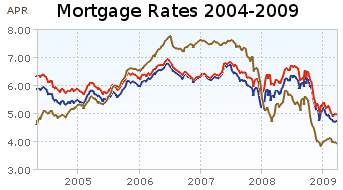

Showing mortgage rates over the last 5 years. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate. From Yahoo Finance, for conventional loans in Virginia.

Showing mortgage rates over the last 5 years. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate. From Yahoo Finance, for conventional loans in Virginia.

The 6 month chart shows that mortgage rates have been declining ever so slightly. Rates on a 1 year adjustable mortgage fell from 5.5 to 4% and have stayed near 4% for all of 2009. 30 and 15 year rates (15 year rates staying about 25 basis points cheaper) have declined from 6.5%, 6 months ago to about 5% at the start of the year and have moved around slightly since. This is while the yield 10 year government treasuries have been rising (normally 30 year fixed rate mortgages track moves in the 10 year government bond). The federal reserve has been buying bonds in order to push down the yield (and stimulate mortgage financing and other borrowing).

Mortgage rates certainly could fall further but the current rates are extremely attractive and I just locked in a mortgage refinance for myself. I am getting a 20 year fixed rate mortgage; I didn’t want to extend the mortgage period by getting another 30 year fixed rate mortgage. For me, the risk of increasing rates outweigh the benefits of picking up a bit lower rate given the current economic conditions. But I can certainly understand the decision to hold out a bit longer in the hopes of getting a better rate. If I had to guess I would say rates will be lower during the next 3 months, but I am not confident enough to hold off, and so I decided to move now.

Related: Mortgage Rates Falling on Fed Housing Focus – posts on mortgages – 30 Year Fixed Mortgage Rates and the Fed Funds Rate – Continued Large Spreads Between Corporate and Government Bond Yields – Lowest 30 Year Fixed Mortgage Rates in 37 Years –

The 2000–2002 bear market had three, with average gains of 21 per cent in the Dow Jones Industrials over 45 days.

The granddaddy of all bear markets, 1929 –1932, had six false alarms with an average gain of 47 per cent. And Japan’s ongoing bear saw the Nikkei rise by at least a third four times in its first four years with 10 more false dawns since then.

Bear markets typically end with a whimper rather than a bang, casting doubt on the latest recovery according to Hussman Econometrics, which analysed numerous US market bottoms and bear market rallies. With the exception of the 1987 crash, the month before the lowest point of a downturn saw a gradual descent.

I don’t put much money on the line trying to time the stock market. I thought the decline was overdone and I have found some things to buy. I am not convinced the current assent of the USA market especially means the bear market is over. If I had to sell stocks, I would be much happier to do it now than 3 months ago. That said, I am not selling anything or reducing my planned buying (401k buying).

Related: Financial Markets Continue Panicky Behavior (Oct 2008) – Trying to Beat the Market – Add to Your 401(k) and IRA – see my investing portfolio results

Consumer borrowing falls in March at fastest pace in over 18 years, Americans saving more

In dollar terms, consumer borrowing plunged by $11.1 billion. That’s the largest dollar amount on records dating to 1943, and more than three times the $3.5 billion drop that economists expected. The borrowing category that includes credit cards dropped 6.8 percent in March after a 12.1 percent plunge in February. The category that includes auto loans fell 4.2 percent after rising by 1.2 percent in February.

The Commerce Department last week said that the personal savings rate edged up to 4.2 percent in March, marking the first time in a decade that the savings rate has been above 4 percent for three straight months.

Good. Consumer debt is far to large and should be paid down. This is a start but a small start, but a much larger reduction in outstanding consumer debt is needed before we have reached a healthy level of debt. The continued improvement in that debt level signifies a stronger economy. Far too many financial journalists instead of pointing out the benefits of such improvement note that this reduces current consumption (and thus, effectively, will lower current GDP – compared to what it would be if we continued to spend beyond our means). You cannot spend money your don’t have forever.

Having more stuff in your house (along with an increased outstanding credit card balance) does not make you economically more successful. And the same holds true for the economy. Having more stuff sitting in people’s house and an increasing debt load is not the sign of a stronger economy (even if it is a route to a higher current GDP). Increased saving and reducing debt will strengthen the economy and improve our economic success over the long term.

Related: Will Americans Actually Save and Worsen the Recession? – Proper credit card use – Personal Saving and Personal Debt in the USA – Americans are Drowning in Debt – Buying Stuff to Feel Powerful

Your Life Insurance Policy May Not Be Protected by Ben Levisohn, Business Week

…

Insurance customers need to be more vigilant. Stop focusing only on cost and service and start worrying about solvency. Check such agencies as Standard & Poor’s (MHP), Fitch Ratings, Moody’s, and A.M. Best to find the highest-rated companies, and be alert for downgrades. Then dig deeper. Find out about an insurer’s exposure to real estate and mortgages and make sure its debt holdings are investment-grade. “Everyone’s under the false assumption that it doesn’t matter what company you buy from,” says Thomas Archer, chairman of financial-services firm Archer Financial Group in New York. “It does.”

• $300,000 in life insurance death benefits

• $100,000 in cash surrender or withdrawal value for life insurance

• $100,000 in withdrawal and cash values for annuities

• $100,000 in health insurance policy benefits

• $300,000 in homeowners benefits

• $300,000 in auto insurance benefits

One option is to diversify your insurance coverage, just like you diversifying investments. Historically insurance company failures have been rare, and even it is even rarer that state funds don’t cover the insurance. But if you have large amounts of insurance you can be a bit safer by having your life insurance needs covered by multiple insurers.

Related: Personal Finance Basics: Long-term Care Insurance – Insurers Raise Fees on Variable Annuities – Personal Finance Basics: Health Insurance – How to Protect Your Financial Health

Read more

Sneaky changes to your credit cards

Credit card interest rates are typically pegged to the prime rate, which has fallen from 5.25% a year ago to 3.25% now. But the national average rate for credit cards has actually risen over that period, moving from 11.3% to 12.4%

…

* The standard balance transfer fee has risen to 3%, and Bank of America recently joined Discover in increasing that fee to 4% on certain offers.

* Cash advance fees had been 3%, but Bank of America now has 5% cash advance fees for money obtained through ATMs and at banks, and 4% fees on advances via direct deposit and checks.

* Foreign transaction fees — charged when you make purchases in other countries or use foreign banks — are going up for many cardholders. Starting June 1, Bank of America will begin charging for a service it had previously provided free: Transactions made in U.S. dollars but processed through foreign banks (such as online purchases from overseas merchants using foreign banks) will be hit with 3% fees.

The incredibly large fees are a good reason to not use your credit card for these activities. 5% to get money from an ATM. You have to be crazy to submit to such a fee. The banks continue to fight with the airlines for who can keep providing the most horrible customer service.

Related: How to avoid getting ripped off by credit card companies – Sneaky Credit Card Fees – Avoid Getting Squeezed by Credit Card Companies – Incredibly Bad Customer Service from Discover Card – more posts on credit cards

Mortgages Falling to 4% Become Bernanke Housing Focus by Brian Louis and Kathleen M. Howley

…

Conventional mortgages averaged 4.61 percent in 1951, 4 percent when backed by the Veterans Administration, and 4.25 percent by the Federal Housing Administration, according to The Postwar Residential Mortgage Market, a 1961 book written by Saul Klaman and published by Princeton University Press. Rates during the 1930s were as high as 7 percent.

…

Mortgages were cheaper through most of the 1940s, ranging from about 4 percent to 5.7 percent, depending on whether the lender was a life insurer, a commercial bank or a savings and loan. In that era, most loans were for 14 years and less.

…

The central bank has purchased more than $300 billion of mortgage-backed securities in 2009 through the week ended April 8, helping to cut home-loan rates to 4.82 percent last week from 5.1 percent at the start of the year, according to Freddie Mac data.

…

The difference between 30-year mortgage rates and 10-year Treasury yields has narrowed to about 2.2 percent from 3.1 percent in December, which was the widest since 1986. The spread remains almost 0.7 percentage point above the average of the past decade, data compiled by Bloomberg show. Rates for 15-year mortgages are about 1.8 percent above 10-year Treasury yields, compared with an average 1.4 percent since 1999.

Excellent article with interesting historical information. I don’t believe mortgage rates will fall to 4% but differences of opinion about the future is one function of markets. Those that predict correctly can make a profit. I am thinking of refinancing a mortgage and I think I am getting close to pulling the trigger. If I was confident they would keep falling I would wait. It just seems to me the huge increase in federal debt and huge outstanding consumer debt along with very low USA saving will not keep interest rates so low. However, as I have mentioned previously, it is interesting that the Fed is directly targeting mortgage rates and possible they can push them lower. The 10 year bond yield has been increasing lately so the slight fall in mortgage rates over the last month are due to the reduced spread (that I can see decreasing – the biggest question for me is how much that spread can decrease).

Related: Fed to Start Buying Treasury Bonds Today – Federal Reserve to Buy $1.2T in Bonds, Mortgage-Backed Securities – Low Mortgage Rates Not Available to Everyone – what do mortgage terms mean?

photo of Cesar Augusto Santamaría Escoto in his welding workshop, Chinandega, Nicaragua.

photo of Cesar Augusto Santamaría Escoto in his welding workshop, Chinandega, Nicaragua.I made my 100th contribution to a micro-loan through Kiva last week. Participating with Kiva is a great antidote to reading about the unethical “leaders” taking huge sums to run their companies into the ground (or even just taking obscene sums to maintain their company). The opportunity to give real capitalists an chance at a better life is wonderful.

Kiva allows you to lend money to entrepreneur (in increments of $25). The most you get back is the amount you loaned, and if the entrepreneur, does not pay back the loan then you take a loss. This is something you do if you believe if giving people an opportunity to make a better life for themselves through hard work and intelligent economic choices.

I encourage you to join me: let me know if you contribute to Kiva and I will add your Kiva page to our list of Curious Cat Kivans. Also join the Curious Cats Kiva Lending Team.

My loans have been made to in 32 countries including: Ghana, Cambodia, Uganda, Viet Nam, Peru, Ukraine, Mongolia, Ecuador and Tajikistan. Kiva provides sector (but I think this data is a not that accurate – it depends on the Kiva partners that are not that accurate on identifying the sectors (it seems to me). A large number of the loans are in retail, clothing and food. I like making loans that will improve productivity (manufacturing, providing productivity enhancing services…) but can’t find as many of those as I would like (8% of my loans are in manufacturing, 11% agriculture, retail 18%, 23% food, 25% services (very questionable – these are normally really retail or food, it seems to me).

Some examples of the entrepreneurs I have lent to: welding workshop (Nicaragua), expanding generator services business with computer services (Cambodia), food production (Ghana), manufacturing nylon (Nigeria), internet cafe (Lebanon), electronics repair (Benin), new engine for mill (Togo), weaving (Indonesia) and a food market (Mexico).

Related: Financial Thanksgiving – MicroFinance Currency Risk – Creating a World Without Poverty – Provide a Helping Hand

21 of my loans have been paid back in full. 3 have defaulted. Those figure give a distorted picture though (I believe). There was a problem with a Kiva partner (they partner with micro-finance banks around the world) MIFEX, in Ecuador. Kiva discovered that MIFEX (i) improperly inflated the loan amounts it posted for entrepreneurs on the Kiva website and (ii) kept the excess amount of the posted loan to fund its own operational expenses. Kiva does not expect any further payments on these loans. I had 2, so I think those 2 give a fair impression. The 3rd default is from Kenya. That loan was to a business selling bicycle parts. In 2008, in Kenya, the prevailing political crisis deteriorated and businesses have either been destroyed or closed in fear of looters. Technically the loan did default, however, I was paid $71.50 out of $75 loan (so the defaulted amount was very small.

Read more

Home Ownership Shelter, or Burden?

The other area of concentrated distress is subprime mortgages, which increased their share of the American mortgage market from 7% in 2001 to over 20% in 2006. According to the Mortgage Bankers Association, the delinquency rate was 22% in the fourth quarter of 2008, compared with only 5% for prime loans.

…

“Perhaps the most compelling argument for housing as a means of wealth accumulation”, argues Richard Green of the University of Southern California, “is that it gives households a default mechanism for savings.” Because people have to pay off a mortgage, they increase their home equity and save more than they otherwise would. This is indeed a strong argument: social-science research finds that people save more if they do so automatically rather than having to choose to set something aside every month.

Yet there are other ways to create “default savings”, such as companies offering automatic deductions to retirement plans. In any case, some of the financial snake oil peddled at the height of the housing bubble was bad for saving.

The debate over whether home ownership is a wise investment or not, is contentious (more so in the last year than it was several years ago). I believe in most cases it probably is wise, but there are certainly cases where it is not. If you put yourself in too much debt that is often a big problem. I also think you should save a down payment first. If you are going to move (or have good odds you may want to) then renting is often the better option.

The “default saving” feature is one of the large benefits of home ownership. That benefit is destroyed when you take out loans against the rising value of the house. And in fact this can not just remove the benefit but turn into a negative. If you spend money you should have (increasing your debt) that can not only remove you default saving benefit but actual make your debt situation worse than if you never bought.

Related: Your Home as an Investment – Nearly 10% of Mortgages Delinquent or in Foreclosure – Housing Rents Falling in the USA – Ignorance of Many Mortgage Holders

Life Insurers Profit as Retirees Fear Outliving Cash by Alexis Leondis

…

Payouts among insurers vary significantly, said Weatherford of NAVA. Monthly payments range from $629 to $745 for a $100,000 investment by a 65-year-old male, according to a survey of six issuers by Hueler Companies, a Minneapolis-based data research firm and provider of an independent annuity platform.

An annuity is a comforting in that you cannot outlive your annuity payment. However, there are drawbacks also. Having a portion of retirement financing based on annuity payments does help planning. Social security payments are effectively an annuity (that also increases each year, to counter inflation). While living off social security payments alone is not an enticing prospect, as a portion of a retirement plan those payments can be valuable. If you have a pension that can also serve as an annuity.

It can make sense to put a portion of retirement assets into an annuity however I would limit the amount, myself. And the annuity payout is partially determined by current interest rates, which are very low, and those now the payout rates are low. If interest rates stay low, then you lose nothing but if interest rates increase substantially in the next several year (which is certainly possible) the payout for annuities would likely increase.

Choosing to purchase an annuity is something that should be done after careful study and only once you understand the investment options available to you. Also you need to have saved up substantial retirement saving to take advantage of the option to buy enough monthly income to contribute substantially to your retirement (so don’t forget to do that while you are working).

Related: Many Retirees Face Prospect of Outliving Savings – Spending Guidelines in Retirement – Retirement Tips from TIAA CREF – Social Security Trust Fund

It’s Now a Renter’s Market by Prashant Gopal

…

Oklahoma City, where people spent just 12% of their income on rent, was the most affordable. Other cheap markets included Indianapolis, Denver, Fort Worth, and Cleveland. The least affordable market was New York, where people spent 57% of their income on rent.

Rental markets are driven largely by 2 factors, vacancy rates and jobs. If jobs in a metropolitan area are increasing rents usually increase. If more new apartments are added to the market than jobs (which then increases vacancy rates) this will push down rates. Other factors influence vacancy rates (such as people moving back in with parent, people sharing apartments…). Those factors often are largely influenced by losing jobs in an area.

D.C. apartment market remains strong

…

Rent increases over the past 12 months for all investment grade apartments kept under the long-term average of 4.2 percent per annum, at 0.5 percent since March 2008.

Related: Housing Rents Falling in the USA – Home Values and Rental Rates – Real estate investing articles – Urban Planning – Longer Commutes Translate to Larger Housing Price Declines

Read more